How to Properly Dissolve a Business: A Step-by-Step Guide

Shutting down a business is never easy, but doing it incorrectly may cost you thousands in unexpected taxes, legal fees, and ongoing obligations that can linger for years. Every month, entrepreneurs who thought they had successfully completed their business closing process are surprised by bills for annual reports they never filed, tax liabilities they didn’t anticipate, and penalties from licenses they forgot to cancel. The difference between simply stopping operations and properly dissolving your business entity can mean the difference between a clean break and a financial headache.

When you properly dissolve a business, you complete a legal process that officially terminates your business entity and shields you from future liabilities. Once your business is dissolved, it can no longer operate, and you’re generally protected from ongoing obligations. However, some responsibilities—such as certain debts or legal issues—may still remain, depending on your state, business structure, and your specific circumstances. This guide will walk you through each critical step, ensuring you close your business the right way and avoid costly mistakes with taxes, fees, and filings.

Key Takeaways

-

Properly dissolving your business is essential to protect yourself from ongoing tax obligations, penalties, and potential legal claims—even after operations have ceased

-

Following a compliant, well-documented process—including filing Articles of Dissolution, settling debts, and notifying all required agencies—helps ensure a clean break and peace of mind

-

Skipping steps or missing deadlines can lead to costly surprises, such as continued state fees, tax bills, or personal liability for unresolved debts

-

Professional guidance can help you avoid common pitfalls and ensure your business closure is smooth, compliant, and final

Understanding Why Proper Dissolution Matters

Without proper dissolution, you'll keep receiving bills for annual reports, franchise taxes, taxes owed, and registration fees—even if your business has stopped operating. Unpaid fees and penalties can quickly add up, and many states will eventually initiate administrative dissolution, which can harm your business credit and reputation.

The IRS also expects you to file final tax returns and properly notify them when closing your business. Dissolution documents become part of the public record once filed with the state. If you fail to file these documents, your business remains legally active, leaving you responsible for ongoing taxes, annual reports, fees, and potential penalties.

As the business attorneys at Scarinci Hollenbeck, LLC explain, "If a business dissolution is not handled properly, you could face significant liability after you close your doors... Failure to properly dissolve a business can result in the business being considered active by the state, which entails continued compliance with state requirements, including filing annual reports and paying state taxes."

InCorp's business dissolution services ensure every requirement is met, protecting you from hidden fees, tax obligations, and lingering liabilities.

Step 1 – Review Your Business Entity Type and Governing Documents

Before starting the dissolution process, it's important to understand how the type of legal entity you're closing—such as a limited liability company (LLC) or a corporation—will affect the process. Each legal entity has its own general requirements and procedures for dissolution, while each individual company or organization may also have specific steps or conditions outlined in its governing documents, such as operating agreements or bylaws.

According to business attorneys at Surovell Isaacs & Levy PLC, "The dissolution process varies depending on the business structure and the terms outlined in governing documents, such as partnership agreements or corporate bylaws." Reviewing your entity type's requirements for dissolution and your internal documents will ensure your company follows the correct steps and avoids complications.

Entity Type Matters

The dissolution process varies significantly depending on your business type. A sole proprietorship simply requires stopping operations since there's no separate legal entity to dissolve, while a limited liability company (LLC) or a corporation requires filing articles of dissolution with the state and has specific tax considerations. Understanding your entity type is crucial because following the wrong dissolution process can result in incomplete closure and ongoing liabilities.

Check Internal Agreements

Your operating agreement, partnership agreement, or corporate bylaws contain information about how dissolution must be handled. These documents often specify voting thresholds required to approve dissolution, methods for distributing remaining assets, and any notice requirements.

Step 2 – Vote to Dissolve the Business

For most businesses with multiple owners, a formal vote is legally required to approve dissolution. Shareholders or partners must document their decisions with written consent or meeting minutes to ensure the process is official and compliant.

Hold a Formal Vote

The dissolution vote process varies by business structure. Corporations usually need a board resolution and shareholder approval, while LLCs require member consent. Partners vote in partnerships. Most states set a required majority—often two-thirds or more—and the vote can take place at a meeting or through written consent.

Record the Decision

Document the dissolution vote in meeting minutes or a formal resolution, noting the date and results. Keep this record as part of your company's legal and compliance files.

Step 3 – File Articles of Dissolution with Your State

To formally dissolve your business, file the Articles of Dissolution with your state government—usually through the Secretary of State. Form names, required fees, and filing methods (file online or by mail) vary by state, so check your state's specific process before submitting your paperwork.

Locate State Filing Requirements

Each state has its own local state filing requirements, dissolution forms, fees, and procedures. Visit your Secretary of State's website to find the correct requirements for your business type. Requirements, fees, and processing times can vary widely, so review your state's instructions carefully.

Submit the Articles

Submit your Articles of Dissolution online or by mail, following your state's instructions. Double-check that your business name, EIN, and registered agent details are correct before filing. Be sure to include the required fee, which varies by state. If you need to make any corrections to your business information before filing dissolution paperwork, you may need to file amendments to your articles first.

Processing usually takes anywhere from a few days to a few weeks. Once approved, you'll receive official confirmation from the state—keep this for your records. If you don't hear back in the expected timeframe, contact your state's office to check your status.

Step 4 – Cancel Registrations, Permits, and Licenses

Your business likely holds various local, state, and federal registrations, permits, and licenses that must be formally canceled to avoid ongoing renewal fees or legal exposure. Trade names (DBAs or fictitious business names) are typically not included in the dissolution process and may require separate action to ensure your business identity is properly closed out and you remain in compliance. Failing to cancel these items can result in unnecessary costs or continued legal obligations.

Cancel Local and State Licenses

To properly close your business, you must cancel local and state licenses. Make sure you determine all of the local and state licenses and permits your business holds, such as sales tax permits, health department licenses, and city business licenses. Notify each local agency directly to request cancellation, and always obtain written confirmation for your records.

Cancel Federal Licenses or Industry Permits

If your business operates in a regulated industry—such as alcohol, tobacco, firearms, trucking, or financial services—you must cancel any federal licenses or special permits. Contact the relevant federal agency directly to complete the process. For example, alcohol and tobacco permits can be terminated through the Alcohol and Tobacco Tax and Trade Bureau (TTB). Always obtain written confirmation from the agency to ensure your business is fully closed out at the federal level.

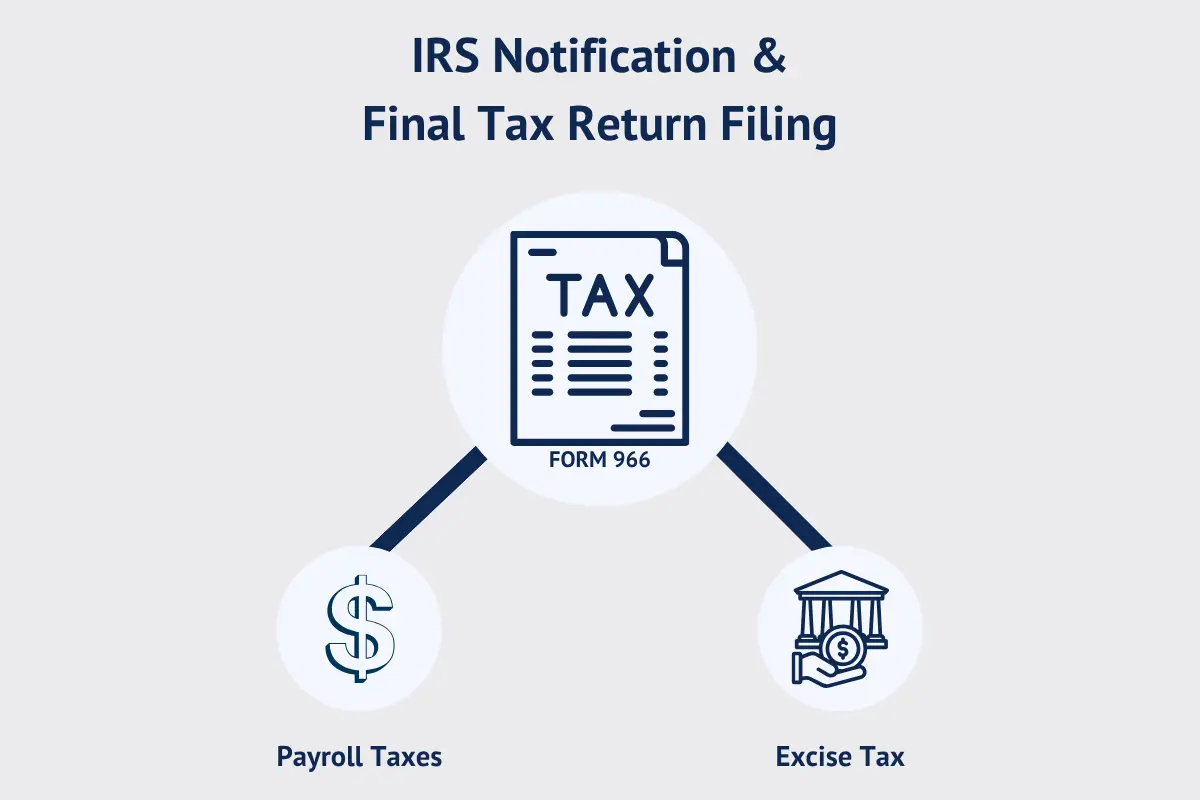

Step 5 – Notify the IRS and File Final Tax Returns

When closing your business, you must file final federal (and, if required, state) tax returns and indicate on the forms that this is your last return. Corporations are also required to file IRS Form 966 within 30 days of adopting a resolution to dissolve or liquidate, notifying the IRS of their intent to close and helping ensure all tax obligations are met.

In addition to your final income tax return, you may need to file other forms to report payroll, excise, or other outstanding tax obligations. For example, if your business sold or stopped using certain business property, you may have to file Form 4797. As the IRS explains, "You also need to file this form if closing your business causes the business use of an eligible property under Section 179 to drop to 50% or less."

Refer to the IRS and state tax agency requirements to ensure you file all necessary documents for your business type.

Mark Final Return on IRS Forms

When you close your business, your final tax return must be clearly marked as a "final return." Most IRS business tax forms—such as Form 1120 for corporations, Form 1120-S for S corporations, Form 1065 for partnerships and multi-member LLCs, and Schedule C for sole proprietors and single-member LLCs—have a checkbox or space labeled "final return." Be sure to check this box or indicate "final" on your last filing for your business type.

If you file other required forms, like employment tax (Form 941) or sales tax returns, follow IRS or state instructions to indicate closure or final status. Marking your returns as final notifies tax authorities that your business has ceased operations and helps prevent future filing obligations.

Cancel EIN (Optional)

While not required, deactivating your employer identification number (EIN) with the IRS can help prevent identity theft or future tax issues. To do this, send a written letter to the IRS, including your business's legal name, EIN, address, and the reason for closure. If possible, include a copy of your original EIN assignment notice. The IRS will confirm the deactivation by mail, and your EIN will remain permanently linked to your business but will no longer be active for tax filings.

Step 6 – Settle Debts and Distribute Remaining Assets

Before distributing any remaining assets to owners or shareholders, you must pay off all business debts—including creditors, lenders, and employees—in the proper legal order. Only after all obligations are satisfied can you divide the remaining assets according to your ownership agreement.

Clear Business Debts First

All business debts and obligations must be paid before distributing any assets to owners. Payments are made in a specific legal order: secured creditors are paid first, followed by employee wages and benefits, then tax authorities, and finally unsecured creditors. Only after these debts are settled can any remaining assets be distributed to owners or shareholders.

Distribute Remaining Assets

Once all debts are paid, distribute any remaining assets to owners based on your ownership agreement, capital accounts (for LLCs and partnerships), or shares (for corporations). Be sure to document all distributions carefully for your records and future tax reporting. If you're unsure how to allocate assets, consult your operating agreement or a qualified accountant or attorney to ensure compliance.

Step 7 – Close Business Bank Accounts and Cancel Business Credit Cards

Ensure all business transactions are complete before closing your business account and canceling business credit cards. Keep copies of your final statements for your records, and formally close any merchant accounts or lines of credit.

Step 8 – Retain Key Business Records

Even after dissolution, you're required to retain key business records for at least 3–7 years, according to IRS guidelines. This includes final tax returns, financial statements, contracts, employee records, and dissolution documents.

Common Mistakes to Avoid When Dissolving a Business

The most common dissolution mistakes include:

-

Failing to file articles of dissolution with the state

-

Neglecting to cancel business licenses, permits, or registrations

-

Incomplete tax filings or failing to file required final tax forms with the IRS (such as final returns or Form 966 for corporations)

-

Distributing assets before paying all debts and creditors

-

Not notifying creditors, employees, or other key stakeholders

-

Overlooking requirements in your operating agreement or bylaws

Note: Failing to complete all legal steps can result in ongoing obligations for your business, such as continued tax liabilities, regulatory penalties, or even personal liability for owners. Carefully review your governing documents, notify all stakeholders, and consult professionals as needed to avoid costly delays or penalties.

Legal and Financial Professionals Who Can Help

Complex dissolutions benefit from professional guidance, including consulting an accountant for tax matters and an attorney for legal compliance. Consider professional help if your business has outstanding debts, employees, or operates in multiple states. Small business owners can especially benefit from expert advice during dissolution.

As the Small Business Administration advises, "Before terminating your lease, selling equipment, and disconnecting utilities, talk to your lawyer and accountant. They'll help you develop a plan to present to creditors, whose cooperation you need during this process."

Final Thoughts on Dissolving a Business the Right Way

Properly dissolving your business requires attention to legal, tax, and administrative details. Taking shortcuts can create long-term problems that are far more expensive than doing it right the first time. Approach dissolution as a professional wrap-up to protect yourself from future liabilities.

Key actions to take:

-

Follow a step-by-step legal process, including filing Articles of Dissolution

-

Notify state agencies, the IRS, and all stakeholders

-

Settle outstanding debts before distributing assets

-

Pay final taxes and file all required tax returns

-

Cancel licenses, permits, and close business accounts

-

Retain key business records for at least 3–7 years

-

Consult legal or tax professionals for guidance and peace of mind

By following these steps, you'll ensure your business is dissolved properly and you're protected from future issues.

FAQs

Do I need to notify the IRS when I close my business?

Yes. You must file your final tax returns marked "final." It's also recommended to notify the IRS in writing to close your EIN account.

How do I cancel a business license or permit after closure?

Contact the issuing agency directly—this may involve submitting a formal request online, by mail, or by phone, depending on the agency's process.

What happens if I don't file Articles of Dissolution with the state?

You may face continued tax obligations, late fees, or legal issues—even if your business has stopped operating.

Can I dissolve my business if I still have debts?

Yes, but you must settle all outstanding debts in the correct legal order before distributing any remaining assets to owners.

How much does it cost to dissolve an LLC in NC?

North Carolina charges a $30 filing fee for LLC dissolution; expedited processing may cost extra.

How long does it take to dissolve a business officially?

It typically takes from a few days to several weeks to voluntarily dissolve your business after filing the Articles of Dissolution with the state. Processing times vary depending on your state and business type, but prompt filing and completing all required steps can help avoid unnecessary delays.

Dissolve Your Business with Confidence and Compliance

Closing a business is a big step—make it a smooth transition by following a clear, well-documented process. Minimize risk and protect your peace of mind by partnering with experienced professionals who can guide you through every detail.

Ready to dissolve your business the right way? Contact InCorp today for expert support and a seamless, compliant closure.

Share This Article:

Stay in the know!

Join our newsletter for special offers.