Understanding UCC Filings: What Businesses Should Know

What if a single document could unlock funding for your company, or block it for years, without you even realizing it? Many business owners have never heard of UCC filings, yet these legal notices play an important behind-the-scenes role in almost every big financing decision. The Uniform Commercial Code, or UCC, sets up a transparent system that protects both borrowers and lenders. These legal notices protect lenders by publicly securing claims on collateral, while also enabling business owners to understand and manage their financing options with greater confidence. In this article, we'll explain what UCC filings are and how understanding them can help you take control of accessing funding for your business.

Key Takeaways

-

What Are UCC Filings? UCC filings (the UCC financing statement, also called a UCC-1 financing statement) are public legal documents that show when a lender has a legal claim on a borrower's property or assets used as collateral. They help protect lenders by making these claims known to everyone, which is important if the borrower doesn't repay a loan

-

For business owners seeking funding: UCC filings are public records that can affect your ability to get loans and show who has a legal claim on your assets. Knowing how these filings work helps you avoid problems and protect your business's credit

-

For lenders: UCC filings let lenders officially claim a legal right to collateral, giving them priority if a borrower doesn't pay. Filing on time helps protect these rights and reduces risk

-

The Uniform Commercial Code (UCC) sets clear, consistent rules for these filings across all states, making lending and borrowing more predictable

-

When both borrowers and lenders handle UCC filings openly and responsibly, it builds trust and stability in business lending

What Is a UCC Filing?

A UCC filing is a legal document that publicly notifies others of when a lender asserts a security interest in a borrower's assets used as collateral. For example, if your business takes out a loan to buy equipment, the lender might file a UCC notice to let others know they have a legal claim on that equipment until the loan is paid off.

The Uniform Commercial Code (UCC) is a set of laws adopted by all U.S. states to standardize commercial transactions, ensuring that a UCC financing statement filed in one state follows similar rules as in any other.

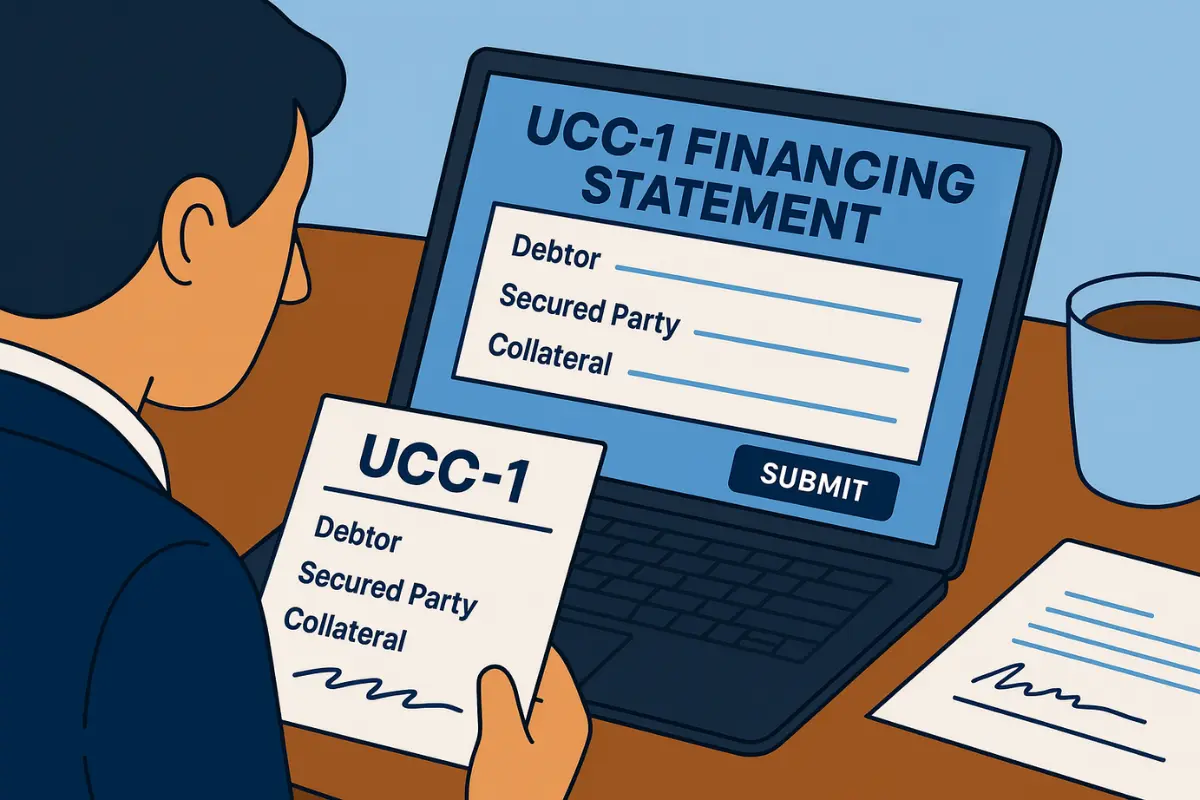

The most common UCC filing is the UCC-1 Statement, which includes key details such as the debtor's name and address, the lender's (secured party) information, and a description of the collateral involved. The debtor may be a person or a business; filings are typically made in the state where the individual or business is located or registered.

Lenders usually file a UCC-1 Financing Statement with the Secretary of State's office when a business obtains equipment financing or other secured loans. By filing this document publicly, the lender officially announces their claim to the collateral. This helps protect both sides by making clear that the lender has priority over other creditors if the borrower defaults.

Why UCC Filings Matter for Your Business

From a borrower’s perspective: UCC filings play a central role in commercial lending by showing lenders what claims already exist on your business assets. Just as entrepreneurs must carefully choose the best business structure to position their company for funding, understanding UCC filings is equally crucial to securing and protecting that financing. When you apply for loans or vendor credit, lenders check UCC records to see if you have existing liens or collateral commitments.

These filings establish priority among creditors; the first lender to file a UCC claim usually holds "first position," giving them the strongest right to the collateral if the borrower defaults. This legal framework protects lenders and helps organize how business debts are handled.

For business owners, multiple or active UCC filings can affect your creditworthiness and financing options. Having many liens on your assets might signal risk to potential lenders, leading to tougher approval processes or higher interest rates. According to Crestmont Capital, "Having a UCC filing on your credit report will not impact your credit score. However, it can impact your chances of qualifying for other forms of financing in the future. [...] It can impact your borrowing power if you have an outstanding loan that has a UCC filing against the business. The bank will want it paid off or you will be offered business loans for bad credit."

Mishandling UCC filings is a common financial mistake many new businesses make. By understanding and properly managing these filings, you can reduce risks and maintain better access to funding.

Types of UCC Filings

The UCC system includes several types of filings that support different stages of secured transactions, from the initial filing to modifications and termination. The specific types and procedures can vary depending on the transaction and state requirements. Each type serves a distinct purpose in managing secured transactions and ensuring proper public notice.

UCC-1 Financing Statement

The UCC-1 financing statement is the initial filing a lender uses to publicly declare their legal claim on a borrower's assets. Lenders typically submit the UCC-1 before providing loan funds to create a public record of their security interest and establish priority over the specified collateral.

This document must include accurate debtor details, such as the exact legal business name registered with the state, following the instructions provided by the filing office. The UCC-1 filing protects the lender's rights by creating a legal claim that generally lasts for five years from the filing date.

UCC-3 Amendment or Termination

The UCC-3 form is used to modify or terminate an existing UCC-1 filing. Lenders file a UCC-3 to correct information like debtor names, update collateral details, or officially release their security interest when loans are repaid.

The UCC-3 also covers other actions, including continuing a filing to extend its effectiveness and assigning rights to another secured party. Termination filings formally release the lender's claim on collateral, clearing public records and restoring the debtor's full ownership rights.

Continuation and Assignment Filings

A continuation filing extends the protection of the original UCC-1 financing statement beyond its standard five-year expiration, allowing lenders to renew their UCC lien and maintain priority. To be effective, the continuation statement must be filed within six months before the UCC-1 expires.

Assignment filings transfer the secured party's interest from one lender to another. This often happens when loans are sold or transferred between financial institutions, ensuring the new lender's claim on the collateral is properly recorded.

Together, these filings help keep UCC records current and protect lenders' rights throughout the lifespan of secured loans.

Who Should File a UCC-1 Financing Statement?

From a lender’s perspective: The secured party, typically the lender, creditor, or financing company, bears primary responsibility for filing UCC financing statements to protect their legal interest in the borrower's collateral. Lenders file UCC-1 statements in various scenarios, including equipment financing arrangements, working capital loans secured by inventory, and vendor credit agreements that extend payment terms.

As Finally, a financial services company explains, "By filing a UCC financing statement, creditors provide public notice of their security interest, enabling them to take possession of and sell specified assets to recover the debt in case of default."

In some cases, debtors may be involved in the filing process, particularly when providing information about collateral locations or business operations across multiple states. However, the secured party maintains ultimate responsibility for ensuring accurate and timely filings.

From a borrower’s perspective: Business owners should understand that UCC filings are a standard practice in commercial lending and reflect the formal processes that underpin relationships with institutional lenders. By managing UCC filings efficiently, businesses can spend less time on administrative tasks and focus more on serving their customers and growing their operations.

Why Should I File a UCC-1 Financing Statement?

From a lender’s perspective: Filing a UCC-1 financing statement establishes a public record that legally protects your security interest in a debtor's assets, creating enforceable rights recognized by the courts. The filing establishes legal priority based on timing, meaning the first secured party to file typically holds superior rights to the collateral over other creditors.

According to legal technology company Litera, "The filing of a UCC financial statement creates a hierarchy of which assets can be seized, and in what order, should the debtor default or declare bankruptcy. For instance, if a borrower takes out another loan from a second lender using the same assets as collateral, the second lender will not be permitted to recover the assets until the first lender is fully satisfied." This protects lenders and suppliers by clearly defining priority and reducing financial risk.

For example, if you lend money to a business and use their equipment as collateral, filing a UCC-1 lets everyone know you have a legal claim to that equipment. This means if the business doesn't repay you, you have priority over other creditors to recover the equipment or its value.

How to File a UCC-1 Financing Statement

From a lender’s perspective: File a UCC-1 Financing Statement by gathering essential information such as the debtor's exact legal name, the secured party's details, and a description of the collateral. Complete all required sections of the UCC-1 form accurately, then submit it along with the nominal fee to your state's Secretary of State office.

Most states offer online filing systems through their Secretary of State websites, though some also accept filings by mail or fax. Filing costs vary by state but generally range from $20 to $120. Your filing will request and notify other creditors of your secured interest, so be sure to fill out all required fields carefully to avoid common errors that could delay or invalidate your filing.

How to Search for Existing UCC Filings

From a lender’s perspective: Before extending credit, conducting a UCC search helps identify existing claims on a debtor's assets and assess available collateral. Most states offer online search systems through their Secretary of State websites, where you can search using key details such as the debtor's name, business name, or file number. These official state databases provide reliable, publicly accessible UCC filing records that are essential for due diligence.

Trusted third-party services can also conduct a UCC search on your behalf. They offer comprehensive reports, including searches of multiple name variations and detailed analysis of existing security interests. Regular UCC monitoring enables businesses to track their own public records and spot unauthorized filings promptly.

How Long Does a UCC Filing Last?

UCC-1 financing statements remain effective for five years from the filing date, after which they automatically expire unless the secured party files a continuation statement. The duration of UCC-1 filings creates predictable expiration dates that help maintain clean public records.

Continuation statements must be filed within six months before the original expiration date to maintain uninterrupted protection. When borrowers repay their loans, the secured party should file a UCC-3 termination statement to formally release their claim.

When Should You File or Terminate a UCC Statement?

From a lender’s perspective: File UCC-1 financing statements before disbursing loan funds or delivering goods to ensure maximum legal protection. Early filing establishes priority over subsequent creditors and secures your interest in the collateral.

Terminate UCC filings promptly after borrowers repay their obligations or when the secured interest no longer applies to maintain accurate and up-to-date public records. Monitor expiration dates and file continuation statements well in advance to avoid gaps in protection and preserve your security interest.

FAQs

Is a UCC filing public information?

Yes, UCC filings are public records accessible through state government databases, typically via the Secretary of State's website, where anyone can search and view documents filed across multiple pages within the system according to state laws.

Can a UCC filing impact my ability to get future loans?

Yes, existing UCC filings may influence loan approval decisions and terms, as they indicate existing claims on your assets that reduce available collateral for new lenders seeking to secure their interest and manage risk among other creditors.

Do I need an attorney to file a UCC-1?

While not legally required, professional guidance ensures accuracy and compliance with complex filing requirements across many states, potentially saving costly corrections when you need to fill out forms or submit documents.

What does a UCC filing cover?

UCC filings typically cover specific collateral such as equipment, inventory, accounts receivable, or other business property used to secure loans through the filing system to notify other creditors and establish priority over personal property.

Can a UCC filing be disputed or removed?

Yes, incorrect or invalid filings can be challenged through termination statements, correction documents, or legal proceedings, depending on the specific circumstances and laws governing such disputes in your jurisdiction.

Final Thoughts: Mastering UCC Filings to Protect and Grow Your Business

From a borrower’s perspective: Beginning with legally naming your business to securing the right insurance, entrepreneurs face many critical steps when starting and managing a business. One often overlooked but essential element is understanding UCC filings. Knowing how UCC filings work empowers business owners to confidently navigate commercial financing while maintaining accurate public records. This transparency benefits the entire commercial lending ecosystem by reducing uncertainty and establishing clear frameworks for secured transactions.

From a lender’s perspective: To protect your security interests effectively, it’s important to be proactive in managing UCC filings. Stay current with UCC searches and filings, and consider consulting legal or financial professionals who can help navigate the complexities and ensure accuracy. Utilizing expert UCC search and filing services, such as those offered by InCorp, can simplify this process, help maintain your priority rights, and strengthen your loan protections.

Share This Article:

Stay in the know!

Join our newsletter for special offers.