Single-Member LLC vs. Multi-Member LLC: Choose the Right Structure

A tech entrepreneur preparing to launch a software company spent weeks debating whether to bring on a co-founder. She worried about sharing control but recognized her gaps in marketing and sales. After consulting advisors, she learned the choice between Single-Member LLC vs Multi-Member LLC structures would affect not just ownership but also taxes, management flexibility, and growth potential. Understanding the Single-Member LLC vs Multi-Member LLC differences before filing formation documents would determine her company's operational framework for years.

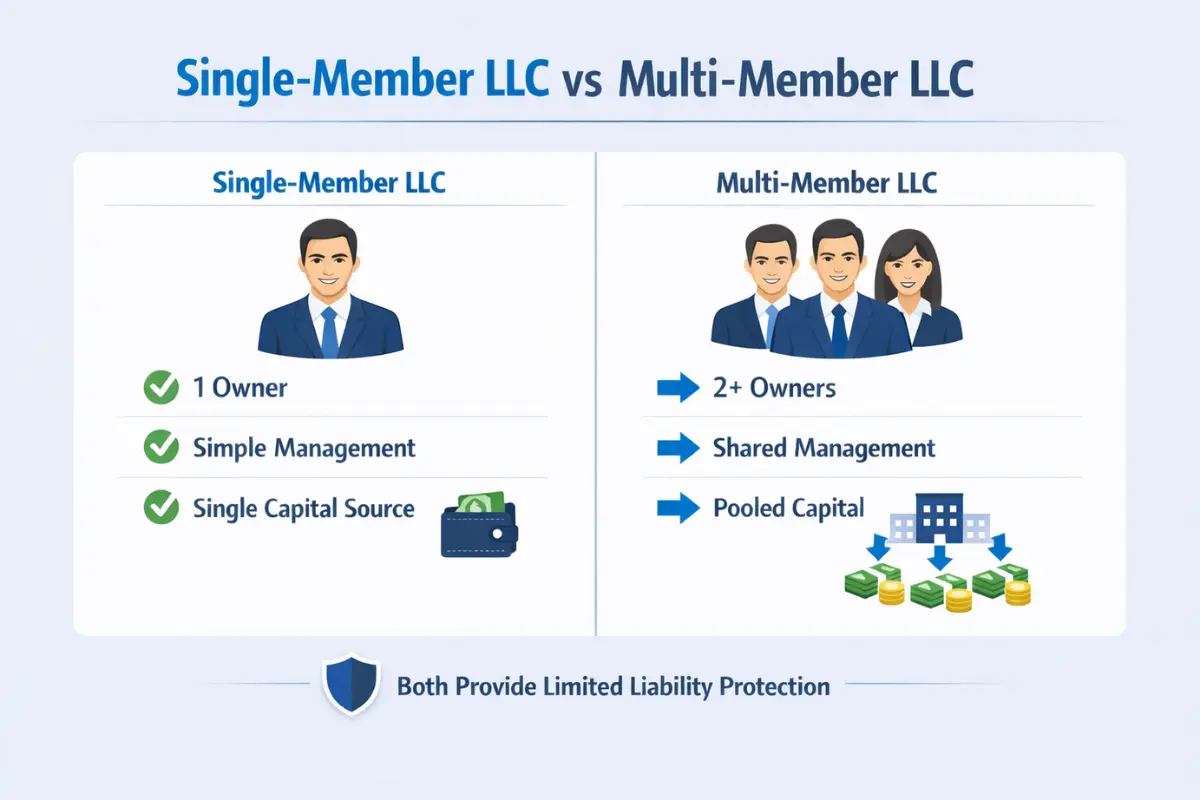

Limited Liability Companies (LLCs) provide a flexible business structure that offers personal liability protection for owners. The primary difference between Single-Member LLCs (SMLLCs), which have one owner, and Multi-Member LLCs (MMLLCs), which have two or more owners, extends beyond simple ownership numbers. Choosing between these structures depends on the entities' management needs, capital requirements, and long-term growth objectives.

Understanding LLC structures helps entrepreneurs select formations aligning with their business models. The right structure provides operational efficiency while maintaining legal protections and tax advantages supporting sustainable growth. Each structure serves different business situations and owner preferences.

Key Takeaways

-

Single-member LLCs (SMLLCs) give one owner full control, simpler decision-making, and streamlined administration, making them well-suited for solo entrepreneurs and independent professionals.

-

Multi-member LLCs (MMLLCs) allow multiple owners to share capital, expertise, risks, and responsibilities, which can support larger or faster-growing businesses.

-

Both SMLLCs and MMLLCs generally offer similar limited liability protection, but specific creditor remedies and charging order protections can vary significantly by state.

-

Tax treatment differs by default: SMLLCs are usually taxed as disregarded entities reported on the owner’s personal return, while MMLLCs are typically taxed as partnerships filing Form 1065 with K‑1s.

-

Either structure can elect alternative tax classifications (such as S‑corporation or C‑corporation status), which may change compliance obligations and tax-planning opportunities.

-

Operating agreements are essential for both structures but are more complex for MMLLCs because they must address voting rights, profit allocations, exits, and dispute resolution among multiple members.

-

MMLLCs often scale more easily when adding partners or investors, while SMLLCs prioritize simplicity for founders who value autonomy and do not anticipate near‑term co‑owners.

-

Choosing between SMLLC and MMLLC should reflect the owner’s control preferences, capital needs, risk tolerance, succession plans, and long‑term business goals, ideally with guidance from qualified professionals.

Understanding the Single-Member LLC (SMLLC)

A single-member LLC is an entity owned by one individual or a business entity, offering total control over all decisions. This structure is often preferred by independent contractors, consultants, and solo entrepreneurs who do not require outside partners. Forbes explains that single-member LLCs combine liability protection with operational simplicity.

SMLLCs provide personal asset protection similar to corporations while maintaining pass-through taxation benefits. The sole business owner makes all strategic and operational decisions without consulting partners or holding formal meetings. This autonomy is valuable for entrepreneurs with clear visions that require quick execution without delays from consensus-building.

Formation requires filing Articles of Organization with state authorities and paying applicable fees. While LLC Operating Agreement documents are not always legally required for SMLLCs, creating them helps maintain the corporate veil that separates business and personal assets. These agreements demonstrate that entities operate as legitimate businesses rather than as alter egos of their owners.

Simplicity in Decision-Making

Owners do not need to consult with partners or hold formal meetings to take action. Every business decision, from signing contracts to adjusting strategies, falls within the sole owners' authority. This streamlined decision-making enables rapid responses to market changes and opportunities without delays in coordination.

LLC management types for SMLLCs inherently involve member-managed structures where owners handle daily operations. No voting procedures or dispute resolution mechanisms are necessary because only one person makes decisions. This simplicity reduces administrative overhead and accelerates business operations.

The absence of partner disagreements eliminates potential sources of business disruption. Owners pursue their visions without compromise or negotiation. However, this also means owners bear sole responsibility for mistakes and cannot share decision-making burdens during challenging periods.

Streamlined Administrative Requirements

While LLC operating agreements are recommended to help maintain the corporate veil, internal governance is less complex than that of multi-owner structures. SMLLCs typically maintain simpler record-keeping systems because they do not track multiple ownership stakes, profit distributions to various parties, or member voting records.

Annual reports and state compliance requirements—including annual reports, registered agent maintenance, and state filing fees—apply identically to single and multi-member LLCs. However, internal documentation requirements remain minimal for SMLLCs. No member meeting minutes are required; partnership disputes need no documentation; and ownership percentage tracking is unnecessary with sole ownership.

Administrative simplicity extends to banking and accounting. With one owner making all decisions and controlling all funds, financial tracking focuses on separating business from personal expenses rather than allocating funds among multiple parties.

Understanding the Multi-Member LLC (MMLLC)

A multi-member LLC is an entity with multiple owners who share risks, rewards, and management responsibilities. This structure suits business partners, family-owned businesses, or groups of investors. MMLLCs distribute ownership through membership interests, which define each member's stake in the entity.

MMLLCs allow flexible governance structures. Members can participate actively in operations or serve as passive investors, depending on the operating agreement's provisions. This flexibility accommodates various partnership arrangements from equal partners to silent investor relationships. LLC ownership structures offer scalability as businesses grow and member roles evolve.

Formation follows processes similar to those of SMLLCs but requires more detailed documentation that addresses multiple-party relationships. Registered agent requirements apply equally to both structures, ensuring that entities maintain proper state registration and service-of-process capabilities.

Shared Capital and Resources

Pooling funds from multiple members helps entities fund larger operations or acquisitions. Rather than relying on single individuals' financial resources, MMLLCs access combined capital from all members. This aggregated capital base supports more ambitious projects than a single owner could typically fund independently.

Operational resources extend beyond financial capital to include time, expertise, and networks. Multiple members contribute diverse skills and professional connections, benefiting business development. One member's marketing expertise complements another's technical skills, creating more comprehensive organizational capabilities.

Capital contributions need not be equal among members. Operating agreements can specify varying contribution amounts with corresponding ownership stakes reflecting each member's financial input. Some members might contribute primarily capital, while others provide primarily expertise, with ownership structures reflecting these different contribution types.

Diverse Expertise and Skill Sets

Having multiple members allows businesses to benefit from various professional backgrounds and viewpoints. Different perspectives help identify blind spots and generate more creative solutions than a single viewpoint can. Strategic discussions incorporating multiple viewpoints often yield more robust business strategies.

Understanding business partnerships reveals how diverse member skills create competitive advantages. Technical founders paired with business-oriented partners often build stronger companies than either could alone. This complementary expertise is particularly valuable in complex industries that require multiple specialized knowledge areas.

Decision-making benefits from diverse input but can slow processes that require consensus. Operating agreements should balance leveraging multiple perspectives with maintaining efficient operations by establishing clear decision-making procedures and delegating authority.

Comparing Liability Protections

Both structures provide the same baseline of limited liability protection, separating personal assets from business debts. LLC liability protection shields members' personal property from business creditors in most situations. This protection represents the primary reasons entrepreneurs choose LLC structures over sole proprietorships or general partnerships.

"Charging order protection", which prevents members' personal creditors from seizing business assets, can vary by state. Some states (such as Texas, Delaware, and Nevada) provide stronger charging order protection for MMLLCs than for SMLLCs, while most states treat both structures equally.

Maintaining "corporate veils" through separate banking and proper filings helps preserve these protections for both LLC types. Commingling business and personal funds, failing to maintain proper records, or using business entities for personal purposes can pierce protective veils, exposing personal assets to business liabilities.

Tax Treatment and IRS Classifications

The IRS views these two entities differently for federal tax purposes. LLC tax classification significantly affects administrative requirements and potential tax-planning opportunities. Understanding default classifications and available elections helps owners optimize tax positions.

Tax Filing complexity varies substantially between structures. Single-member LLCs face simpler requirements with Schedule C reporting, while multi-member LLCs must file partnership returns (Form 1065) with K-1s for each member. The IRS notes that if the LLC is a corporation, normal corporate tax rules apply, and it should file Form 1120, U.S. Corporation Income Tax Return.

Both structures can elect alternative tax treatments if beneficial. SMLLCs can elect corporate taxation, while MMLLCs can choose S-corporation or C-corporation status. These elections require filing appropriate forms with the IRS and may trigger different administrative and tax obligations.

SMLLC as a Disregarded Entity

The IRS automatically treats solo LLCs as "disregarded entities," with income reported on owners' personal tax returns (Schedule C). Business profits and losses flow directly to owners' Form 1040 returns without separate business-level returns. This pass-through taxation avoids double taxation affecting C-corporations.

Schedule C reporting proves relatively straightforward compared to partnership returns. Owners report business income alongside other personal income sources, calculating self-employment tax on net business earnings. No separate business tax return filing is required unless owners elect corporate tax treatment.

Tax Advantages of disregarded entity status include simplified filing and the avoidance of separate business-level taxation. However, all business income is subject to self-employment tax, which can be costly for profitable businesses. S-corporation elections may reduce self-employment tax burdens for some SMLLCs.

MMLLC as a Partnership

The IRS treats multi-member LLCs as partnerships by default, requiring separate information returns (Form 1065) and K-1s for each member. Partnership tax return filings report business income and expenses, then allocate profits and losses to members through Schedule K-1 forms, which members include in personal returns.

Each member reports their allocated share of profits or losses on personal tax returns regardless of whether they actually received distributions. This means members may owe taxes on business profits even if entities retain earnings for reinvestment rather than distributing them.

Partnership taxation allows flexible profit-and-loss allocations that are not strictly tied to ownership percentages. Operating agreements can specify special allocations rewarding members' different contributions or roles. However, allocations must have "substantial economic effect" under IRS regulations to receive tax recognition.

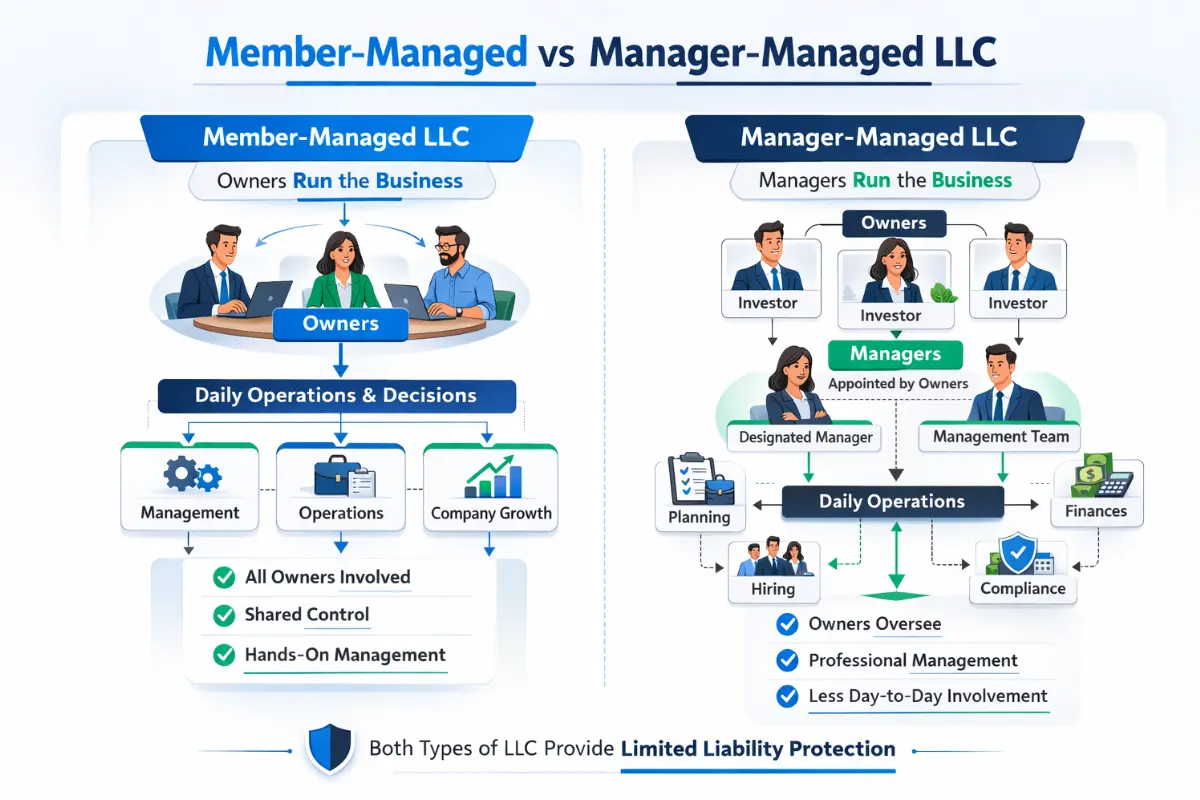

Management Styles: Member-Managed vs. Manager-Managed

Both SMLLCs and MMLLCs can choose how businesses are run on a daily basis. LLC management types fall into two categories: member-managed, in which all owners participate in daily operations, and manager-managed, in which members appoint individuals to handle the entity's affairs.

The SBA explains that member-managed structures are suitable for smaller LLCs in which all members actively participate. Manager-managed structures work better when some members are passive investors or when businesses require professional management expertise that members lack.

Management structure choices should reflect members' time availability, expertise, and preferences for involvement. Active members wanting control typically prefer member-managed structures, while busy professionals with limited time for daily operations often choose manager-managed arrangements.

Operational Flexibility and Scaling

Each structure handles growth and the addition of new stakeholders differently. Single-member LLCs must convert to multi-member LLCs if taking on partners or investors. This conversion requires amending operating agreements, updating state filings, and changing tax treatment from disregarded entity to partnership status.

Multi-member LLCs are built to scale, as operating agreements typically already include provisions for admitting new members. Adding members requires following the procedures outlined in existing agreements rather than restructuring entire entities. This built-in scalability proves valuable for businesses anticipating growth or additional capital needs.

Understanding business formation helps entrepreneurs plan for future growth when selecting initial structures. Businesses anticipating rapid expansion or external investment often choose multi-member structures from the outset, even with few members, to facilitate future additions.

Complexity of the Operating Agreement

While both should have operating agreements, documents for MMLLCs are significantly more detailed. LLC operating agreement complexity correlates with the number of members and potential complications from multiple-party relationships. Single-member agreements primarily establish entities' separate legal status and basic operating procedures.

MMLLC agreements must address profit distributions, voting rights, and "buy-sell" provisions preventing future disputes. These documents specify how members make decisions, resolve disagreements, handle member exits, and manage other potential conflict situations. Well-drafted agreements anticipate problems before they arise.

For SMLLCs, agreements primarily serve to reinforce entities' separate legal status in the eyes of the courts. These documents demonstrate that owners treat businesses as legitimate entities rather than personal activities. While simpler than multi-member agreements, they still provide valuable legal protections.

Compliance and Filing Requirements

Both SMLLCs and MMLLCs face similar state-level compliance tasks, such as maintaining registered agent presence and filing annual reports. States impose identical requirements regardless of member numbers. Failure to meet these state requirements can lead to loss of good standing for either entity type.

LLC compliance requirements include maintaining up-to-date information with the states, paying annual fees, and ensuring that registered agent services remain active. Both structures must obtain the required business licenses and permits before operating. Compliance obligations apply equally across LLC types.

Commercial registered agent services help both solo and multi-member entities stay on top of varying deadlines across states. Professional agents ensure that entities receive important notices and maintain good standing, supporting continued operations and legal protections.

Business Continuity and Succession Planning

MMLLCs offer natural continuity: if one member leaves, the business often continues under the remaining members. Operating agreements typically include provisions for member withdrawals, deaths, or incapacities that specify how interests transfer and how businesses continue. This built-in succession planning provides stability during ownership transitions.

Contrast this with SMLLCs, where deaths or incapacities of sole owners may lead to business dissolution in some states if successors are not clearly named in operating agreements or estate planning documents. Without designated successors, businesses may cease operations or face complex probate proceedings. Single-member LLC owners should establish clear succession plans protecting business continuity.

Having formal plans in place helps protect entities' long-term stability regardless of structure. Succession planning is particularly important for businesses with significant value, ongoing client relationships, or employees who depend on continued operations. Both structures benefit from documented succession strategies.

Costs of Formation and Maintenance

State filing fees for Articles of Organization are generally the same regardless of the number of members. Formation costs primarily consist of state filing fees, registered agent services, and any professional fees for legal or formation assistance. These initial costs typically range from several hundred to several thousand dollars, depending on the state and service provider.

MMLLCs may incur higher professional fees for tax preparation and legal drafting due to the complexity of partnership filings and multi-party agreements. Annual accounting and tax preparation costs typically exceed SMLLC costs due to partnership return requirements and multiple K-1s.

Choosing structures should be based on long-term value and risk mitigation rather than initial setup costs alone. Slightly higher ongoing costs for MMLLCs may be worthwhile for businesses that benefit from multiple members' capital, expertise, and shared responsibilities. Cost considerations should weigh against strategic benefits.

Key Decision Factors When Choosing LLC Structure

Several considerations beyond basic ownership numbers should inform structure selection. Business stage, industry requirements, funding needs, and personal preferences all influence which structure best serves specific situations. Evaluating these factors systematically helps entrepreneurs make informed choices.

Current business needs may differ from future requirements. While starting as an SMLLC provides simplicity, businesses anticipating partner additions or investor fundraising might benefit from initial multi-member structures. Conversely, solo entrepreneurs committed to maintaining sole ownership benefit from the simplicity of an SMLLC without unnecessary complexity.

Industry norms and expectations sometimes favor particular structures. Professional service providers often operate as SMLLCs until their practices expand and warrant partners. Technology startups frequently begin as MMLLCs, anticipating co-founder arrangements and future funding rounds requiring multiple members.

Evaluating Control Preferences

Entrepreneurs must honestly assess their comfort with shared decision-making. Some founders thrive on collaboration and value diverse perspectives. Others prefer autonomous control and find consensus-building frustrating. These personality factors significantly affect satisfaction with chosen structures.

Control preferences extend beyond daily operations to strategic decisions. SMLLCs grant complete autonomy over changes in business direction, major expenditures, and strategic pivots. MMLLCs require members' agreement for significant decisions unless the operating agreements specify otherwise.

Relinquishing control proves difficult for many entrepreneurs, even when they recognize partners' value. Before forming MMLLCs, potential members should discuss their decision-making philosophies, conflict-resolution approaches, and acceptable levels of compromise. Misaligned expectations about control often cause partnership failures.

Assessing Financial Requirements

Capital needs substantially influence the choice of structure. Businesses that require significant startup capital or ongoing funding benefit from pooled resources. SMLLCs limit capital to the single owner's personal resources and to external financing they can secure independently.

Revenue projections and profitability timelines also matter. Businesses expecting to reach profitability in years may need multiple members to share financial burdens during the startup phase. Quickly profitable businesses requiring minimal capital investment work well as SMLLCs.

Exit strategies affect structure appropriateness. Businesses planning to sell to larger companies or considering public offerings may benefit from multi-member structures that facilitate complex ownership transitions. SMLLCs work well for lifestyle business owners who plan to operate indefinitely.

Understanding Risk Tolerance

Risk tolerance varies among entrepreneurs. Some accept higher personal financial risks in pursuit of complete control and potential rewards. Others prefer to share risks with partners, even if it means sharing rewards. These preferences should align with structure choices.

MMLLCs distribute risks among members. If businesses fail, losses spread across multiple parties rather than devastating single individuals. However, risk distribution comes with reward sharing; successful businesses split profits among members rather than flowing entirely to sole owners.

Personal financial situations affect appropriate risk levels. Individuals with substantial savings, low personal expenses, or external income sources may comfortably assume SMLLC risks. Those with limited resources, high expenses, or family obligations might benefit from MMLLC risk sharing.

Choose What Fits Your Business Goals

Whether SMLLCs or MMLLCs are "better" depends on the specific goals and management preferences of business owners. The Single-Member LLC vs Multi-Member LLC decision ultimately reflects entrepreneurs' visions for their businesses. Solo entrepreneurs preferring complete control and simplified administration may find single-member structures ideal. Partners who share a vision and complementary skills often thrive in multi-member arrangements.

InCorp's filing services help establish and maintain both single-member and multi-member entities efficiently. Professional formation support ensures proper documentation, state compliance, and structural foundations supporting long-term success. Contact InCorp to explore how professional services support LLC formation.

InCorp's Registered Agent and EntityWatch® services help ensure businesses remain in good standing across all jurisdictions. Ongoing compliance support allows owners to focus on operations while professionals manage state requirements, filings, and notices, ensuring continued legal protections and operational authority.

FAQs

Can a Single-Member LLC have employees?

Yes. Single-member LLCs can hire employees just like any other business entity. Owners must obtain Employer Identification Numbers (EINs), withhold payroll taxes, and comply with employment laws regardless of the number of LLC members.

Can a Multi-Member LLC be owned by other businesses?

Yes. Members can be individuals, corporations, other LLCs, or trusts, depending on state law. This flexibility allows complex ownership structures in which parent companies own subsidiary LLCs or multiple entities share ownership of joint ventures.

Do LLCs need a business bank account?

Yes. Keeping separate business bank accounts helps maintain clear financial boundaries between entities and owners. Understanding the banking requirements for Single-Member LLCs and Multi-Member LLCs is important for preserving liability protections by demonstrating that businesses operate independently of owners' personal affairs.

Can an LLC change its number of members later?

Yes. LLCs can add or remove members as long as state rules and operating agreements allow it. Adding members converts SMLLCs to MMLLCs, requiring tax status changes and agreement amendments. Member exits require the following buyout procedures specified in operating agreements.

When should I choose a member-managed LLC versus a manager-managed LLC?

Member-managed LLCs work best when all LLC members actively participate in day-to-day operations and decision-making. Manager-managed LLCs are better when some owners are passive investors or when the business needs centralized management, allowing one or a few managers to run operations while other members have more limited, high-level roles.

How does an operating agreement affect liability protection in a single-member or multi-member LLC?

A well-drafted operating agreement helps show that the LLC is a separate legal entity, supporting limited liability protection for both single-member and multi-member structures. It clarifies management structure, profit distribution, and procedures for business operations, which reduces the risk that a court views the LLC as the owner's "alter ego."

Do tax implications differ significantly between single-member and multi-member LLCs?

Yes. For tax purposes, a single-member LLC owned by an individual is usually treated as a disregarded entity, with business income reported on Schedule C of the owner's personal tax return. A multi-member LLC is typically taxed as a partnership, filing Form 1065 and issuing K‑1s to members, though both types can elect S corporation or C corporation status if that better aligns with their tax strategy.

What banking and compliance steps help preserve limited liability protection for any LLC structure?

Every LLC, whether single-member or with multiple members, should open a dedicated business bank account, keep personal and business finances separate, obtain an Employer Identification Number when required, and maintain required business licenses and annual reports. These steps support the LLC's status as a separate legal entity and help protect personal assets from business debts and liabilities.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.