LLC vs Sole Proprietorship: Differences You Need To Know

A freelance graphic designer operating under her own name for three years earned a steady income but hesitated to pursue larger corporate clients. When a Fortune 500 company requested her services, its legal department required proof of formal business registration and liability insurance before signing the contract. The LLC vs sole proprietorship decision became clear: the $40,000 contract required the credibility and asset protection only an LLC could provide.

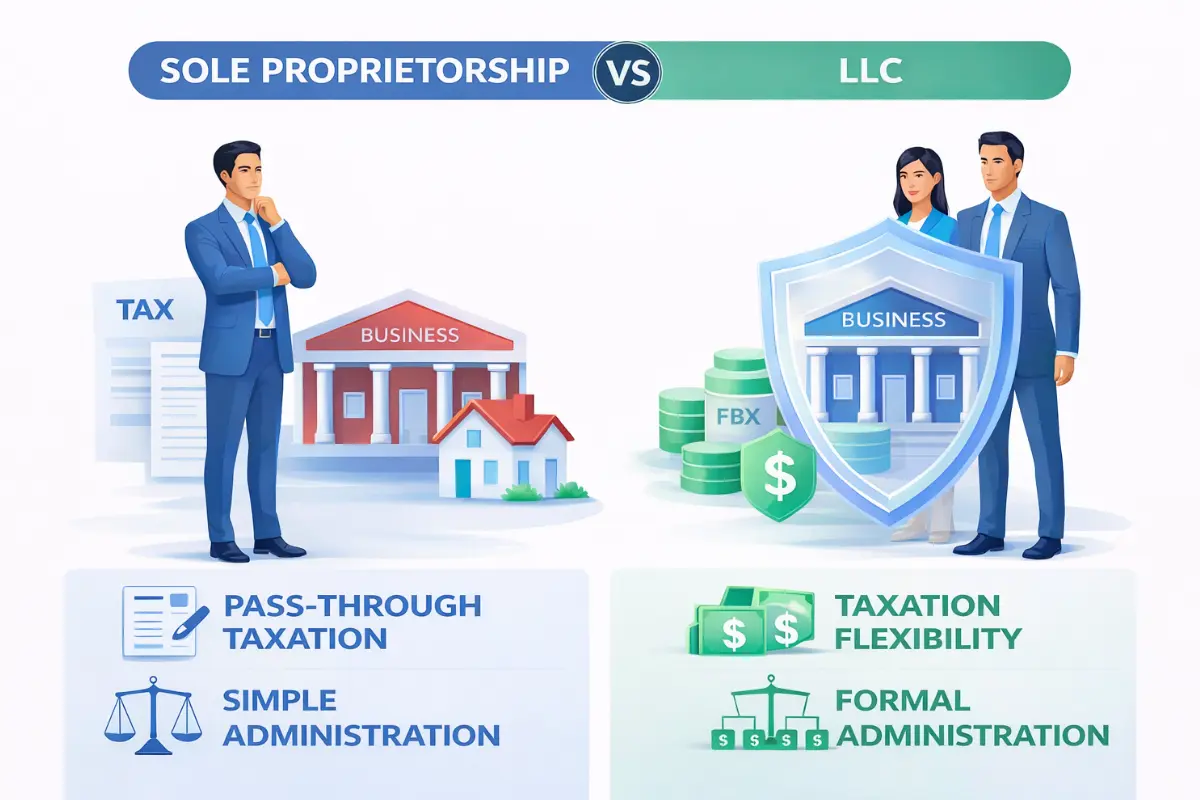

The fundamental choice for single-owner businesses is to remain a default sole proprietorship or formally register as a Limited Liability Company. The primary difference centers on legal entity separation—whether the law views you and your business as one person or as two distinct entities. While both structures remain common for startups in 2026, this decision affects asset protection, tax options, and administrative overhead.

According to the U.S. Small Business Administration, sole proprietorships account for the majority of small businesses in the United States. This prevalence stems from the structure's automatic formation and zero startup costs. Understanding the business structure comparison between these two options helps entrepreneurs make informed decisions aligned with their risk tolerance, growth plans, and asset protection needs.

Key Takeaways

-

A sole proprietorship is the default for one-owner businesses, offering simple setup and full control but exposing your personal assets to all business debts and lawsuits.

-

An LLC creates a separate legal entity, which generally shields your home, savings, and other personal property from business liabilities as long as you keep finances separate and maintain required filings.

-

Both structures use pass‑through taxation by default, but only LLCs can elect S‑corp or C‑corp status, which can reduce self‑employment tax for higher‑profit businesses when set up correctly.

-

Sole proprietorships are cheaper and easier to start, while LLCs involve formation fees, annual reports, and more administration in exchange for stronger liability protection and increased credibility with banks and corporate clients.

-

Owners who plan to pursue larger contracts, raise capital, or build a long‑term, transferrable business often benefit from starting—or eventually converting—to an LLC rather than staying a sole proprietor indefinitely.

Legal Identity and Personal Liability

The "unincorporated" nature of a sole proprietorship contrasts with the "separate legal entity" status of an LLC. This distinction determines whether creditors can pursue your personal assets when business obligations arise. Understanding the benefits of an LLC vs. a sole proprietorship requires examining how courts treat each structure.

Sole Proprietorship: Unlimited Personal Liability

The law views the owner and the business as a single legal unit. No separation exists between business assets and personal assets, meaning business liability extends directly to the owner's personal property. Personal assets, including your home, car, and bank accounts, can be seized to satisfy business debts or legal judgments.

If a client sues your sole proprietorship and wins a judgment, creditors can pursue your personal savings accounts, place liens on your home, and garnish future wages. This unlimited liability exposure represents the most significant risk of operating without formal entity protection.

Insurance policies can mitigate some risks, but coverage gaps and policy limits leave substantial exposure. Sole proprietors working in high-risk industries face the greatest risk of personal asset protection failures.

LLC: Limited Liability Protection

The LLC operates as a separate legal person that enters into its own contracts and incurs its own debts. This separation shields owners from personal responsibility for most business obligations.

An owner's financial risk typically remains limited to the amount invested in the business. If the LLC faces a $100,000 lawsuit but only holds $15,000 in assets, the member's personal assets generally remain protected. Creditors can pursue the LLC's business property, but cannot automatically reach the member's home or personal accounts.

A single-member LLC receives the same liability protection as multi-member LLCs. The key lies in proper entity maintenance—keeping business finances separate, maintaining required filings, and operating in accordance with the operating agreement.

Important exceptions exist. Members remain personally liable for their own wrongful acts. Personal guarantees on business loans create direct liability regardless of LLC status. Failing to maintain corporate formalities—such as commingling funds or ignoring required filings—can result in "piercing the corporate veil," thereby eliminating liability protection.

Formation and Administrative Requirements

The "automatic" start of a sole proprietorship contrasts with the formal registration required for an LLC. Understanding the benefits of forming an LLC requires weighing administrative requirements against the protections gained.

Minimal Setup for Sole Proprietors

No formal state filing is required to start a sole proprietorship—the business exists once commercial activity begins. This simplicity makes sole proprietorships attractive for testing business concepts with minimal upfront investment, as outlined by IRS guidelines for sole proprietorships.

A "Doing Business As" (DBA) name is often the only required filing when the owner doesn't use their legal name. Understanding DBA vs LLC helps clarify that a DBA provides name registration without creating entity separation or liability protection.

Business registration for sole proprietors typically includes obtaining necessary business licenses and permits. These requirements vary by industry and location but apply regardless of business structure. The minimal setup costs make sole proprietorships accessible—beyond potential DBA fees of $10 to $100, sole proprietors face no entity formation costs.

Formal Registration for LLCs

LLCs require filing Articles of Organization with the state, appointing a Registered Agent, and paying state filing fees ranging from $50 to $500. The Articles of Organization establish the LLC's legal existence and include the business name, registered agent information, and member details.

Many business owners use professional registered agent services, such as InCorp's business services, to ensure reliable mail handling and maintain privacy.

Maintaining a separate business bank account becomes essential for preserving legal integrity. Commingling personal and business funds undermines LLC protection. Creating an operating agreement provides crucial governance documentation outlining ownership, profit distribution, and management responsibilities.

Ongoing business compliance requirements include annual reports, franchise taxes, and license renewals. Most states require LLCs to file periodic reports updating member information. Failure to submit these filings can result in administrative dissolution, eliminating liability protection. Annual compliance costs typically range from $50 to $800.

Taxation and Filing Flexibility

The pass-through taxation nature remains common to both structures while highlighting the unique flexibility available only to LLCs. Pass-through entities report business income on owners' personal returns. For 2026, tax optimization remains a primary reason businesses choose LLCs over sole proprietorships.

Default Pass-Through Treatment

Both structures report business profits on the owner's personal Form 1040 using Schedule C filing by default. This pass-through treatment means business income flows directly to the owner's personal tax return without taxation at the business level.

Owners of both structures are subject to self-employment taxes on all net business profits. The self-employment tax rate of 15.3% covers Social Security (12.4%) and Medicare (2.9%) contributions.

The EIN vs. SSN question varies by structure. Sole proprietors without employees can use their Social Security Number, while LLCs typically obtain an Employer Identification Number. An EIN provides better privacy protection and facilitates banking relationships.

Both structures claim identical business deductions on Schedule C. The deduction opportunities remain the same—the difference lies in tax flexibility beyond the default treatment.

The LLC's "Tax Flexibility" Advantage

Unlike sole proprietors, LLCs can elect to be taxed as an S-Corp or C-Corp through an S corporation election with the IRS. Sole proprietorships cannot make these elections—they remain locked into pass-through taxation with full self-employment tax exposure.

An S-Corp election can help high-earning owners save on self-employment taxes by splitting income between salary and distributions. The owner pays themselves a "reasonable salary," subject to payroll taxes, and then takes additional profits as distributions, taxed only at income tax. For a business netting $150,000 annually, this election might save $8,000 to $12,000.

The LLC tax benefits extend beyond S-Corp elections. LLCs can also elect C-Corp taxation in specific situations. The administrative burden increases,, but the tax savings often justify the added complexity for businesses with annual profits exceeding $60,000 to $80,000.

Business Continuity and Credibility

How external parties perceive the two structures reveals critical differences for growth-oriented businesses. Understanding business continuity planning helps entrepreneurs structure for long-term success.

Credibility with Lenders and Clients

An LLC is often viewed as more "permanent" and professional by banks, vendors, and high-value clients. Financial institutions perceive LLCs as serious business entities, which translates into better access to business credit lines and more favorable lending terms.

Sole proprietors may find it difficult to secure large corporate contracts. Many corporations require vendors to maintain formal business structures and liability insurance before awarding contracts.

The best business structure for a small business often depends on the target clientele. Service providers targeting individual consumers may operate successfully as sole proprietors, while businesses pursuing corporate contracts typically benefit from forming an LLC.

Perpetual Existence vs. Termination

A sole proprietorship legally ceases to exist upon the owner's death or retirement. The business has no independent existence beyond the owner.

An LLC can have perpetual existence, allowing smoother transfer of ownership or sale. The operating agreement can include succession provisions designating who inherits membership interests. This continuity protects business value and maintains client relationships.

The ability to transfer ownership represents another advantage. Sole proprietors can only sell assets and client lists, while LLC members can sell membership interests, transferring ownership of an ongoing entity with established contracts and licenses intact.

Summary Comparison Table: LLC vs. Sole Proprietorship

| Feature | Sole Proprietorship | Limited Liability Company (LLC) |

|---|---|---|

| Legal Separation | None | Separate Legal Entity |

| Personal Liability | Unlimited | Limited (Asset Protection) |

| Formation Cost | $0 (except for DBA/Licenses) | $50 - $500+ (plus annual fees) |

| Tax Flexibility | Pass-Through Only | Pass-Through, S-Corp, or C-Corp |

| Administrative Burden | Minimal | Moderate (Annual Reports/Fees) |

| Credibility | Lower | Higher |

Start Your Business with Confidence

While a sole proprietorship offers the easiest start, an LLC provides the structural protection and credibility necessary for a growing business. The choice depends on your industry risk profile, growth plans, asset protection needs, and willingness to maintain compliance requirements.

Entrepreneurs testing business concepts with minimal risk exposure may start as sole proprietors and change sole proprietorship to an LLC once the business gains traction. However, businesses in high-risk industries, those with significant personal assets to protect, or ventures pursuing corporate contracts benefit from forming an LLC immediately.

Understanding LLC formation costs helps with planning. Initial formation expenses include state filing fees, registered agent services, and operating agreement preparation, typically totaling $300 to $1,000 in the first year, with ongoing annual compliance costs of $100 to $500.

Explore InCorp's business services to help move your business beyond the sole proprietorship model. InCorp's LLC formation services include filing Articles of Organization, appointing a registered agent, and monitoring compliance. The EntityWatch® system helps monitor state compliance requirements and protect "Good Standing" status.

InCorp is not a law firm and does not provide legal or financial advice. This information is educational. Readers should consult with qualified legal and tax professionals.

The sole proprietor vs. LLC taxes decision extends beyond current-year savings to long-term wealth-building. LLCs preserve the option to optimize tax structure as business income grows, potentially saving tens of thousands in taxes over the business's lifetime.

FAQ's

Can a sole proprietorship have a business license?

Yes. Many states and municipalities require licenses or permits even for sole proprietors operating under their own name or a DBA. Business licensing requirements depend on industry, location, and business activities rather than entity structure. Check with your local city hall, county clerk, and state licensing boards to identify required permits for your specific business activities.

Can an LLC be converted from an existing sole proprietorship?

Yes. A sole proprietorship can form an LLC and transfer assets and operations into the new entity. The how to form an LLC process from an existing sole proprietorship involves filing Articles of Organization, obtaining an EIN, opening a business bank account, and transferring business assets to the LLC. This conversion preserves business continuity while adding liability protection and tax flexibility.

Are there ongoing state fees for sole proprietorships?

Generally, no, unless a DBA or a specific license requires renewal. Sole proprietorships typically have minimal ongoing state fees compared to LLCs. However, business license renewals and industry-specific permits may require periodic fees regardless of structure. Some states charge annual DBA renewal fees ranging from $10 to $50.

Can a sole proprietor hire employees?

Yes. Sole proprietors can hire staff, but they remain personally liable for payroll taxes and business obligations. Hiring employees requires obtaining an EIN, registering for state payroll taxes, withholding income and payroll taxes, and maintaining workers' compensation insurance. The sole proprietor bears personal responsibility for all employment-related liabilities, including wage claims and workplace injuries.

How does personal liability differ between a sole proprietorship and an LLC?

In a sole proprietorship, there is no legal separation between the owner and the business, so the sole proprietor can be held personally liable for business debts, lawsuits, and other business obligations. In a limited liability company (LLC), the company is a separate legal entity, and limited liability protection generally shields the owner's personal assets—like a home or personal savings—from most business debts and claims, as long as business and personal assets are kept separate and the LLC is properly maintained.

How do taxes work for a single-member LLC compared to a sole proprietorship?

For federal income taxes, a single member LLC is typically treated as a "disregarded entity" and taxed the same way as a sole proprietorship, with business profits reported on the owner's personal income tax return and subject to self-employment taxes. The key difference is that an LLC owner can later elect S corporation or C corporation tax status if that better fits their income level and tax planning goals, while a sole proprietor cannot change from default pass-through taxation without first forming a new business entity.

When might a sole proprietorship be the better choice than an LLC?

A sole proprietorship offers the simplest setup and lowest upfront cost, which can be attractive for low risk businesses testing a new business idea or side gig with minimal assets at stake. Many small business owners start as sole proprietors when they have limited business income, few business assets, and are comfortable taking on unlimited liability in exchange for minimal paperwork and no separate business tax return.

What role does an operating agreement play if I'm the sole owner of an LLC?

Even for a single member LLC, an operating agreement documents how business decisions are made, how business profits are handled, and how business and personal assets must remain separate. This internal document supports the legal separation between the LLC and its owner, which can be important for maintaining limited liability protection and showing banks, lenders, or the Internal Revenue Service that the LLC is a formal business structure and not just an unincorporated business.

How do funding and banking typically differ between a sole proprietorship and an LLC?

Sole proprietors often use a personal bank account plus a business DBA account, but they remain personally responsible for all business loans and other business obligations. LLCs are expected to use a dedicated business bank account and business banking products, which helps preserve legal separation and can make it easier to obtain business funding, because lenders view the LLC as a distinct business entity even when there is only one owner.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.