Business Exit Strategy: How to Sell Your LLC and Maximize Value

Every LLC owner exits eventually, whether by choice or by circumstance. The path might be a sale, a transfer to family, an employee buyout, or a quiet wind-down, and the difference between walking away with full value and walking away frustrated usually comes down to one variable: whether the exit was planned. Roughly half of U.S. business owners either expect to close their business outright or have no succession plan at all, which means a sizable share of practices end up worth less than they should be when the moment finally arrives.

For owners who do prepare, the market is genuinely active. Small business acquisitions in the United States totaled 9,546 closed transactions in 2024, a 5% year-over-year increase, with a combined enterprise value of $7.59 billion and a median sale price of $345,000. A clear business exit strategy for selling an LLC is what turns a forced wind-down into one of those numbers, rather than a footnote in someone else’s closure statistics.

This guide maps out the major LLC exit strategy options, the structural choice between an asset sale and a membership interest sale, how to value the entity, and the legal and tax decisions associated with each path. None of what follows is legal or tax advice. Owners should consult qualified attorneys and tax professionals before structuring any sale, since the right move on paper can still go sideways without state-specific guidance.

Key Takeaways

-

A business exit strategy for an LLC works best when planned years in advance, not at the moment of retirement, illness, or burnout, because preparation directly affects sale price and deal terms.

-

Most LLC owners exit through one of four paths—third-party sale, management or employee buyout, family succession, or formal dissolution—and the right choice depends on the operating agreement, financial health, and the owner’s goals.

-

How you sell your LLC (asset sale vs. membership interest sale) can change tax treatment, which contracts and licenses transfer, and which liabilities stay behind, so structure is just as important as valuation.

-

LLC valuation usually starts with earnings using methods like the income and market approaches, with seller’s discretionary earnings and industry multiples anchoring what buyers are willing to pay.

-

Clean financial statements, reduced owner dependency, and good standing with all states where the LLC does business make the company more attractive to buyers and help your small business sell faster.

-

Tax implications of selling an LLC—including capital gains, depreciation recapture, and installment sale treatment—should be modeled with a tax professional before you sign a letter of intent or allocate the purchase price.

Types of LLC Exit Strategies

Four paths cover most LLC exits, and the right one depends less on what is theoretically available and more on what fits the owner’s timeline, the business's financial position, and the language buried in the operating agreement.

Selling to a Third Party

Most owners looking to monetize their business default to a third-party sale, which is the practical way to sell an LLC. Two structural options sit on the table from day one: an asset sale or a membership interest sale, both of which are covered in detail in the next section.

The buyer pool itself splits into two camps. Strategic buyers, meaning competitors or adjacent companies, tend to pay a premium for the LLC’s customer base or market position because the acquisition fits a larger plan. Financial buyers, including private equity firms, care less about strategic fit and more about cash flow predictability, and they price accordingly.

Management or Employee Buyout

When the existing leadership team is the buyer, the deal becomes a management buyout, and the dynamics shift in useful ways. Continuity is largely preserved for employees and customers; institutional knowledge stays put; and the departing owner still gets a defined exit. Financing typically takes the form of installment payments funded by the business’s own cash flow, which means the deal can close without external lenders or the diligence theater that comes with them.

Family Succession

Some owners would rather pass the business to a child or another relative than sell it openly. The transfer can be structured as a gift, a sale, or a mix of both, and the operating agreement should govern how membership interests move within the family rather than leaving it to default state law. The non-financial pieces matter just as much as the structure: who actually wants to run the business, who is ready, and how the rest of the family feels about the choice. Estate and gift tax implications add complexity, and succession planning that begins years in advance generally produces better outcomes than a transfer triggered by a sudden event such as illness or a death in the family. The InCorp overview of how to transfer ownership of an LLC covers the mechanics of transferring LLC ownership for partial transfers and intra-family moves.

Dissolution

Sometimes the math just does not support a sale, and forcing one anyway costs more than it returns. The LLC can then be formally dissolved by winding up its business affairs, settling debts, distributing any remaining assets to its members, and filing dissolution paperwork with the state. The InCorp guide on how to dissolve an LLC walks through the steps. Dissolution typically recovers less value than a sale, so it works best as a fallback rather than a default plan. The U.S. Chamber of Commerce’s tips for creating an exit strategy reinforces what most advisors say plainly: the value of planning ahead compounds, and the cost of skipping it shows up at the worst possible moment.

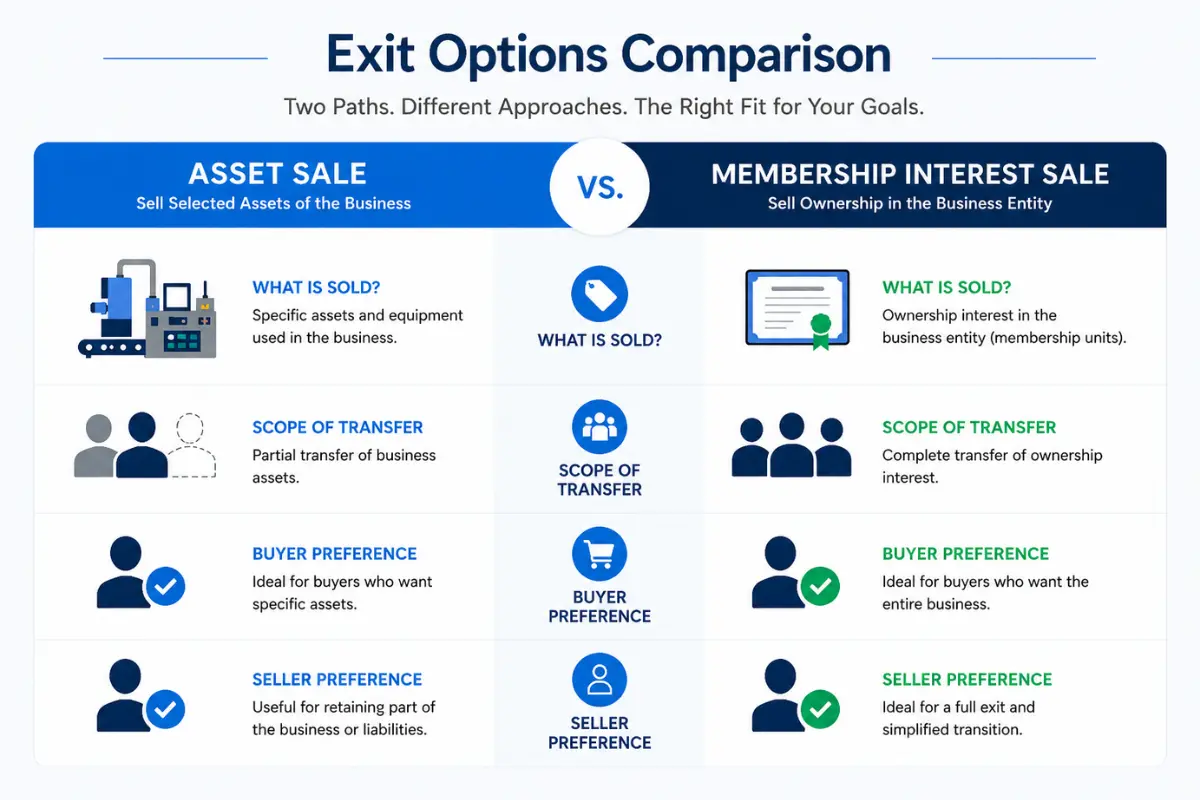

Asset Sale vs. Membership Interest Sale

Few decisions matter more in selling a limited liability company than how the deal is structured, because that single choice ripples through tax treatment, liability exposure, and which contracts and licenses come along for the ride. Buyer and seller usually start from opposite preferences here, which is why the sell LLC assets vs membership interests question gets negotiated alongside price rather than after it.

Asset Sale

In an asset sale, specific business assets transfer to the buyer (equipment, inventory, customer lists, intellectual property, goodwill), and the LLC entity itself stays with the seller. Buyers typically prefer this structure because they get to pick what to acquire and walk away from unknown liabilities, which is exactly the kind of leverage they want in diligence. The tradeoff lands on the seller’s side. Contracts, licenses, and permits often need to be individually reassigned, and that work can extend the timeline by weeks or months, depending on which counterparties have to sign off.

Membership Interest Sale

A membership interest sale works the other way around. The buyer purchases the seller’s ownership stake, and the LLC continues as a going concern with its contracts, tax ID, licenses, and bank accounts intact, which is the cleanest mechanical handoff available. Sellers tend to prefer this route for the simpler mechanics and the more favorable capital gains tax treatment that usually comes with it. Buyers push back, and reasonably so, because they assume every liability of the LLC along with the entity itself. The InCorp overview of selling a corporation vs. selling an LLC covers the structural differences in more detail.

How to Value Your LLC

Three approaches dominate LLC business valuation work: income, market, and asset-based. Which one fits depends on the size, industry, and financial profile of the business, and most professional valuations use one as the primary method and a second as a sanity check. For context on where the small-business market currently sits, the average cash flow multiple for small business sales reached 2.61 in 2025, with median seller’s discretionary earnings of $158,950, so the typical small-business deal lands somewhere around $415,000 in value before adjustments.

Income Approach

Profitable LLCs almost always end up valued on the income approach, because their cash flow is the asset doing the work. The method calculates value from expected future earnings, using either a discounted cash flow analysis or a capitalization-of-earnings method. Smaller businesses typically use seller’s discretionary earnings (SDE) as the base figure, while larger businesses use EBITDA. The earnings figure gets multiplied by an industry multiple, then adjusted for working capital and debt to land on a defensible number a buyer can actually finance.

Market Approach

Comparable-sales analysis sits at the core of the market approach, which values the LLC by reference to similar businesses that recently sold. A business broker or an online comparable-transaction database supplies the underlying multiples, and the resulting number is generally only as good as the comp set behind it. Niche businesses often have thin comparables, which means this approach tends to be more useful as a sanity check on an income-based LLC business valuation than as a standalone method.

Asset-Based Approach

For asset-heavy businesses and LLCs being wound down, the asset-based approach often makes more sense than the income or market approaches. It calculates value as the fair market value of tangible and intangible assets minus liabilities, which provides a floor rather than a ceiling. For most operating businesses with healthy cash flow, the income approach still produces a higher and more defensible business valuation. Whatever method anchors the asking price, a formal business valuation by a credentialed appraiser, or at a minimum, a broker’s opinion of value, is what holds up under buyer scrutiny later.

Preparing Your LLC for Sale

Preparation does more for the eventual sale price than any other variable, and it is also the part most owners underinvest in. Owners who start 12 to 24 months before the planned exit consistently get better terms, faster closings, and fewer last-minute surprises, because the work that used to feel optional becomes leverage when a buyer is at the table.

Clean Up Financial Records

Every line of the financial statements gets scrutinized once a buyer engages, so the records have to be ready before that conversation starts. The standard diligence package includes:

-

Three to five years of business tax returns

-

Profit and loss statements and balance sheets for the same period

-

Accounts receivable and payable aging reports

-

Recasting workpapers that separate personal from business expenses

Most owner-operated LLCs run some personal items through the business, which is normal and not a problem on its own, but it does mean recasting is the only way to give the buyer an accurate view of true profitability.

Reduce Owner Dependency

What a buyer is buying is future cash flow, not the seller’s personal involvement, and a business that runs on the founder’s heroics is a business that prices accordingly. Building a management team, documenting standard operating procedures, and handing off key customer relationships in the year before a sale all lift the valuation ceiling. The transition is also kinder to the owner. A business that runs without daily intervention is one a founder can actually step away from without watching it stumble in the rearview mirror.

Ensure Compliance and Good Standing

Good standing matters before the first buyer call, because diligence questions about it surface fast and missing answers slow everything down. The LLC needs to be current with the state of formation and any foreign-qualified states, with active annual reports, a designated registered agent, and no outstanding fees. A Certificate of Good Standing is almost always requested during due diligence, and it is exactly the kind of document many owners only think about once a buyer asks for one and the timeline tightens.

The kind of quiet background work that keeps an LLC sale-ready, which includes registered agent coverage, annual report filings, Certificate of Good Standing requests, and multi-state compliance tracking, is often easier to outsource than to maintain in-house. InCorp handles each of these through its EntityWatch® compliance system, so good standing stays current rather than catching up under deadline pressure.

Review the Operating Agreement

Pull the operating agreement out of the file before doing anything else, and read it like the buyer’s lawyer will. Common provisions that affect a sale include:

-

A buy-sell agreement that governs how members can exit and how interests are valued

-

Right of first refusal for existing members

-

Restrictions on transfer of membership interests to outside parties

-

Required approval thresholds (majority, supermajority, or unanimous) for a sale

-

Valuation methods under an LLC buy-sell agreement or LLC buyout agreement

Where the operating agreement is silent, default state law fills the gap, and the result is rarely what the owner would have chosen. Reviewing and amending before listing avoids the kind of mid-deal delay that costs leverage and, sometimes, the deal itself. The InCorp guide on whether you need an operating agreement for your LLC covers the basics for owners who never put one in place to begin with.

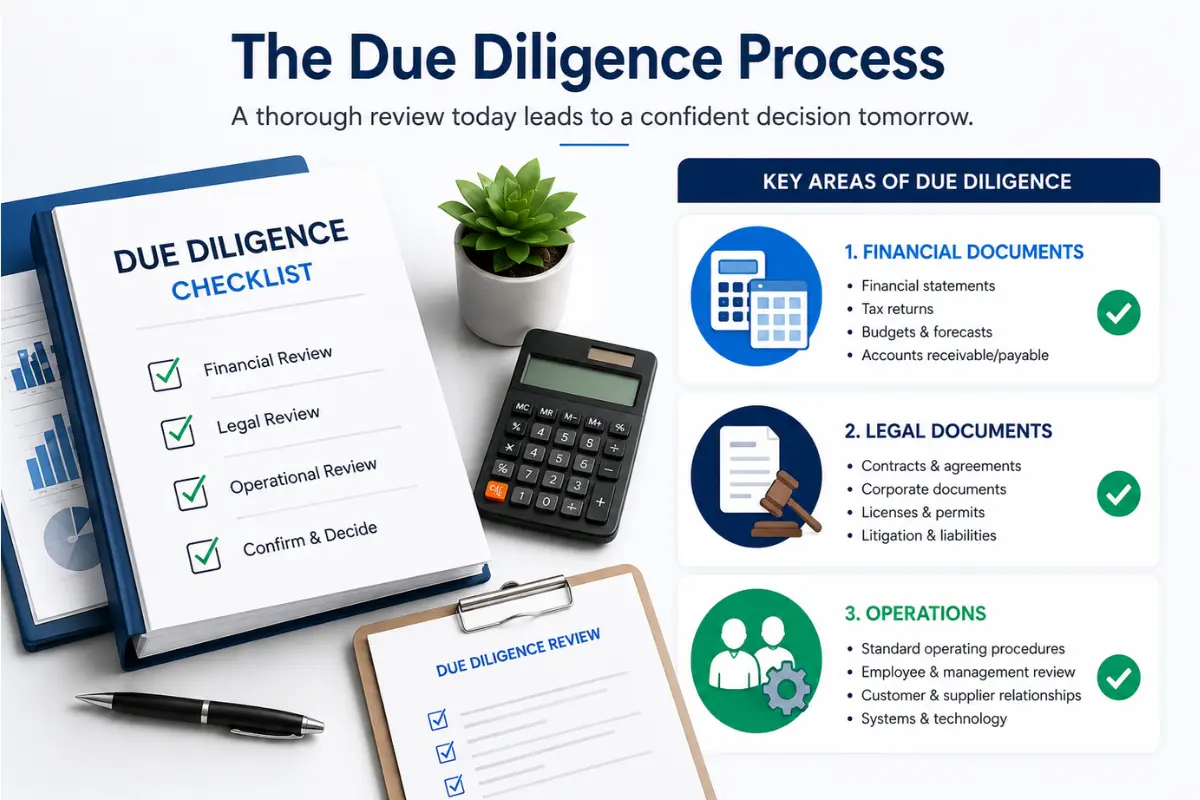

The Due Diligence Process

Due diligence is where buyer verification meets seller representation, and where most deals either harden or unravel. The process typically runs 30 to 90 days and covers the financial, legal, and operational dimensions of the LLC in roughly that order. A signed letter of intent kicks off the diligence period and sets the headline price and structure, both of which remain subject to negotiation of a definitive purchase agreement once the findings come in.

Financial Due Diligence

The numbers get checked first, and they get checked thoroughly. Buyers and their accountants typically request three to five years of tax returns, P&L statements, balance sheets, bank statements, accounts receivable and payable aging, and revenue concentration by customer. Inconsistencies between tax returns and internal financials are the single most common red flag, and they tend to surface late in the process when the seller has the least leverage to explain them.

Legal Due Diligence

Legal review widens the lens beyond the numbers to the operating agreement, articles of organization, material contracts and leases, litigation history, intellectual property, and regulatory compliance. The buyer wants to confirm that the LLC is in good standing and that contracts can be transferred or assigned without counterparty veto. The U.S. Small Business Administration’s overview of how to close or sell your business covers the legal-document checklist most buyers work from, and it is a useful reality check on what the seller will be asked to produce.

Operational Due Diligence

Beyond the numbers and the contracts, operational diligence assesses something harder to quantify: stability. Key employee retention, customer concentration risk, and vendor relationships all get examined, because the buyer is trying to picture the business running without the seller in the chair. Common deal killers include:

-

Customer concentration above 20 to 30% of revenue tied to a single account

-

Key-person dependency on the seller or another individual

-

Undisclosed debts, liens, or pending legal claims

-

Material contracts that prohibit assignment without counterparty consent

Tax Implications of Selling an LLC

How the deal is structured determines how the IRS treats it, and that structural choice has bigger long-term consequences than most price negotiations. The tax implications of selling an LLC turn on the asset sale vs. membership interest sale choice, the LLC’s tax classification (single-member, partnership, or S election), and how the purchase price is allocated across categories. A tax professional should run the structure before either side signs anything binding, because the math after closing rarely favors revisiting.

Membership Interest Sale Tax Treatment

Selling membership interests is generally treated as a capital transaction, which is part of why sellers prefer this structure. Interests held more than one year may qualify for long-term capital gains tax treatment, which is typically lower than ordinary income rates and can preserve a meaningful share of the proceeds. Watch for the "hot assets" rules, though. A portion of the gain may be recharacterized as ordinary income if the LLC holds unrealized receivables or appreciated inventory, and that recharacterization can quietly add five or six figures to the tax bill on a midsize deal.

Asset Sale Tax Treatment

Asset sales require allocation of the purchase price across the individual assets transferred, and each category is taxed on its own terms:

-

Inventory is generally taxed as ordinary income

-

Depreciable equipment may trigger depreciation recapture

-

Real property may qualify for Section 1231 treatment

-

Goodwill is generally taxed as a long-term capital gain

-

Non-compete payments are generally ordinary income to the seller

That allocation is negotiated, not assigned, and it must be reported consistently by both parties on IRS Form 8594. Buyer and seller often want different allocations for tax-efficiency reasons, which is why the allocation discussion happens early and not as paperwork at closing. The IRS overview of the sale of a business covers the allocation framework in more detail.

Installment Sales and Earnouts

Two related structures help bridge financing or valuation gaps when a clean cash deal is not on the table. An installment sale lets the seller receive payment over multiple years and recognize the gain proportionally, which spreads the capital gains tax liability across tax years rather than concentrating it in one (this structure is governed by IRC Section 453). An earnout, by contrast, makes part of the purchase price contingent on post-closing performance targets, which can bridge a valuation gap when buyer and seller disagree on what the business is worth. Earnouts can work well, but they add complexity and tend to generate disputes if expectations are not clearly documented in the purchase agreement, so the language around them deserves disproportionate attention.

Post-Sale Considerations

Closing is not the end, even though it feels like it. A handful of post-sale obligations shape how cleanly the seller transitions out and whether the deal stays clean once the wire hits.

Non-Compete and Transition Agreements

Most buyers will ask for a non-compete agreement at closing, because they are paying for the goodwill and customer relationships and do not want the seller competing for either next month. The typical term is 2 to 5 years within a defined geographic area and industry, though enforceability of a non-compete agreement varies meaningfully by state (California, for example, limits them substantially). A transition services agreement often pairs with the non-compete, under which the seller assists with the operational handoff for 3 to 12 months while the buyer gets up to speed.

State Filings and Entity Updates

Once the deal closes, the LLC may need to file amendments with the state to reflect new ownership, a new registered agent, or updated address information. Where the entity will not be reused after an asset sale, formal dissolution filings end its compliance footprint and stop the meter on annual reports and registered agent fees. InCorp’s corporate dissolution service handles those filings end to end.

Gallup’s polling on the gap in small business succession planning shows how often this final step gets skipped, which is why it deserves a calendar reminder and not an assumption.

Plan Your LLC Exit with Confidence

A successful business exit strategy for selling an LLC starts well before any buyer is in the picture, and the owners who treat it that way consistently capture more value than the ones who improvise. Clean records, a current operating agreement, an active registered agent, and a clear sale structure put the owner in position to capture full value, whatever path the exit takes: third-party sale, buyout, family transfer, or structured dissolution.

InCorp supports owners across that lifecycle with registered agent representation in all 50 states, annual report management, Certificate of Good Standing requests, articles of amendment, and corporate dissolution. The InCorp article on whether you can sell an LLC is a practical starting point for mapping out an LLC exit strategy and the LLC acquisition process.

FAQ's

Can you sell an LLC?

Yes. An LLC can be sold as a membership interest sale, which transfers the entity itself, or as an asset sale, which transfers the underlying assets while the LLC shell stays with the seller. The operating agreement governs the process, including required member approvals, right of first refusal, and any transfer restrictions on outside buyers.

Is it better to sell LLC membership interests or assets?

Each structure has trade-offs. Sellers generally prefer membership interest sales for the simpler mechanics and the capital gains treatment that often follows. Buyers prefer asset sales because they can choose which liabilities to assume and may receive a stepped-up basis. The right answer depends on the specific deal and on professional tax guidance.

How do you value an LLC for sale?

The three primary methods are the income approach (based on earnings), the market approach (comparing to similar sold businesses), and the asset-based approach. For most small businesses, an income-based valuation using a multiple of seller's discretionary earnings is the standard starting point. The 2025 average SDE multiple was 2.61.

What are the tax implications of selling an LLC?

Tax treatment depends on whether the sale is structured as an asset sale or a membership interest sale. Membership interest sales are generally treated as capital gains. Asset sales require allocation of the purchase price across asset categories, with each taxed differently. Installment sales can spread the liability across years.

How long does it take to sell a small business?

The average small business takes about 7 to 9 months from listing to closing. Preparation should begin 12 to 24 months earlier to clean up financials, reduce owner dependency, and resolve compliance issues. Due diligence alone runs 30 to 90 days. Prepared businesses sell faster and at higher valuations.

How does a well‑planned business exit strategy help maximize the value when selling your LLC?

A well‑planned exit strategy gives you time to improve financial performance, document processes, and build a capable management team so the company can operate independently of the owner, which increases perceived value. It also lets you time the business sale to more favorable market conditions and industry trends, instead of being forced to sell when cash flow is weak or external conditions are poor. Clear planning around your financial goals, personal goals, and future growth story makes the business more attractive to prospective buyers and supports a higher, more realistic valuation.

What role does business valuation play in choosing the right exit strategy for my LLC?

Business valuation helps you compare what different exit paths are actually worth in today's market, whether that is a full exit to financial buyers, a sale to a strategic buyer, or a transfer to a family member. Understanding fair market value, liquidation value, and the impact of discounted cash flow or asset‑based valuation methods lets you see how different scenarios affect your financial returns and long‑term goals. A realistic valuation grounded in business performance, predictable earnings, and market conditions makes it easier to pick the exit plan that aligns with both your business journey and your personal objectives.

How do financial performance and cash flow affect the price buyers are willing to pay for my LLC?

Consistent growth, strong cash flow, and clean financial statements give buyers confidence that the business can continue to perform under new ownership, which directly supports a higher business value. Predictable earnings and evidence of operational maturity—like systems, processes, and a capable management team—reduce risk for investors and buyers, which can make a significant difference in both the multiple and the overall sale price. Weak or volatile performance usually results in lower offers, more aggressive due diligence, and more deal terms designed to de‑risk the transaction for the buyer.

What is the difference between asset sales and selling the whole company, and how can that impact my exit plan?

In an asset sale, buyers acquire selected assets such as equipment, customer relationships, and intangible assets like goodwill, while you keep the legal entity, which can influence tax treatment and how much risk each side assumes. Selling the entire company or membership interests typically results in a smoother transition for contracts, employees, and ongoing operations, but it may expose the buyer to more historical liabilities and therefore affect their view of value and risk. Your exit strategy should weigh how each structure affects present value, after‑tax proceeds, and the likelihood of a successful sale to potential buyers in today's market.

How can business owners prepare their company today for a successful exit in the future?

Owners can start de‑risking the business by improving documentation, strengthening financial reporting, and building an organization that can operate independently of the founder, which all support higher value and a smoother transition. Investing in steady, consistent growth, clarifying a compelling future growth story, and aligning the business with industry trends make the company more attractive to both strategic and financial buyers. Early planning also gives you time to align your exit plan with your long‑term personal goals—whether that is a full exit, new ventures, or continued involvement—so that when it is time to sell, you can move through the process with confidence rather than urgency.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.