Family Business LLC: How to Plan for Succession and Build Strong Governance

Family businesses form the backbone of the U.S. economy, contributing 54% of GDP, employing 59% of the workforce, and creating 78% of all new jobs. Yet only about 40% survive to the second generation, 13% to the third, and just 3% to the fourth and beyond. Approximately 70% of global family businesses do not have a formal succession plan, according to the 2019 STEP Global Family Business Survey.

A family business LLC provides a flexible legal framework that helps families establish clear ownership rules, plan for generational transitions, protect personal assets, and preserve generational wealth. InCorp can assist with formation, operating agreement development, and ongoing compliance. This guide covers what a family LLC is, the formation steps, the essentials of an operating agreement, governance structures, succession planning strategies, tax advantages, and protection against family conflicts.

Key Takeaways

-

Family business LLCs give families a flexible way to define ownership, management roles, and profit sharing while protecting personal assets from business liabilities.

-

A detailed operating agreement is the foundation of family governance, covering ownership percentages, voting rights, buy‑sell terms, and dispute‑resolution procedures so conflicts do not derail the business.

-

Early, formal succession planning—using tools like gradual gifting of membership interests, clear succession triggers, and coordinated estate plans—increases the odds that the business survives across generations.

-

Family LLCs can offer meaningful estate and gift tax advantages, including potential valuation discounts and strategic use of annual exclusions and lifetime exemptions, when implemented with professional guidance.

-

Strong governance structures such as manager‑managed LLCs, family councils, and independent advisors help separate family dynamics from business decisions and support long‑term continuity.

What Is a Family Business LLC?

A family business LLC is a limited liability company whose members are related by blood, marriage, or adoption. It provides a legal framework for defining each family member's ownership interest, management responsibilities, and financial rights.

Family LLC benefits include customized ownership percentages, management structures that reflect family dynamics, succession-planning mechanisms, and estate planning through gradual ownership transfer. The structure provides asset protection by separating the business from each member's personal assets.

Family LLCs are used to operate businesses, hold real estate, manage investments, and facilitate estate planning. Understanding what a family LLC is helps families evaluate whether this structure fits their goals.

Benefits of Structuring a Family Business as an LLC

The LLC structure offers distinct advantages for family businesses, combining operational flexibility with asset protection and tax benefits.

Personal Asset Protection

An LLC creates legal separation between family members' personal assets and the business. If the business faces a lawsuit or debt, only LLC assets are typically at risk. This asset protection can help shield personal savings, homes, and other investments.

Maintaining the LLC correctly is essential. Families must maintain separate bank accounts, keep proper records, and avoid commingling personal and business finances. Understanding how to protect personal assets helps families implement comprehensive strategies.

Flexible Ownership and Management

An LLC allows families to customize ownership percentages, management structure, voting rights, and profit distribution to reflect each member's contribution. The operating agreement can grant different classes of membership interests, such as voting versus non-voting memberships.

This flexibility proves valuable when some family members are active in operations while others serve as passive investors.

Tax Flexibility

A family business LLC defaults to pass-through taxation—the business does not pay federal income tax. Profits and losses flow through to each member's personal return based on ownership interest, avoiding double taxation.

Families may benefit from valuation discounts when gifting LLC membership interests, reducing estate and gift tax exposure. Combined discounts of 25% to 45% for lack of marketability and minority interest are common.

Simplified Succession

An LLC structure enables gradual ownership transfer to the next generation without disrupting operations. Membership interests can be gifted over time, and the operating agreement defines how and when transitions occur. This allows founding members to reduce taxable estates while maintaining control. Understanding strategies for family businesses provides additional planning context.

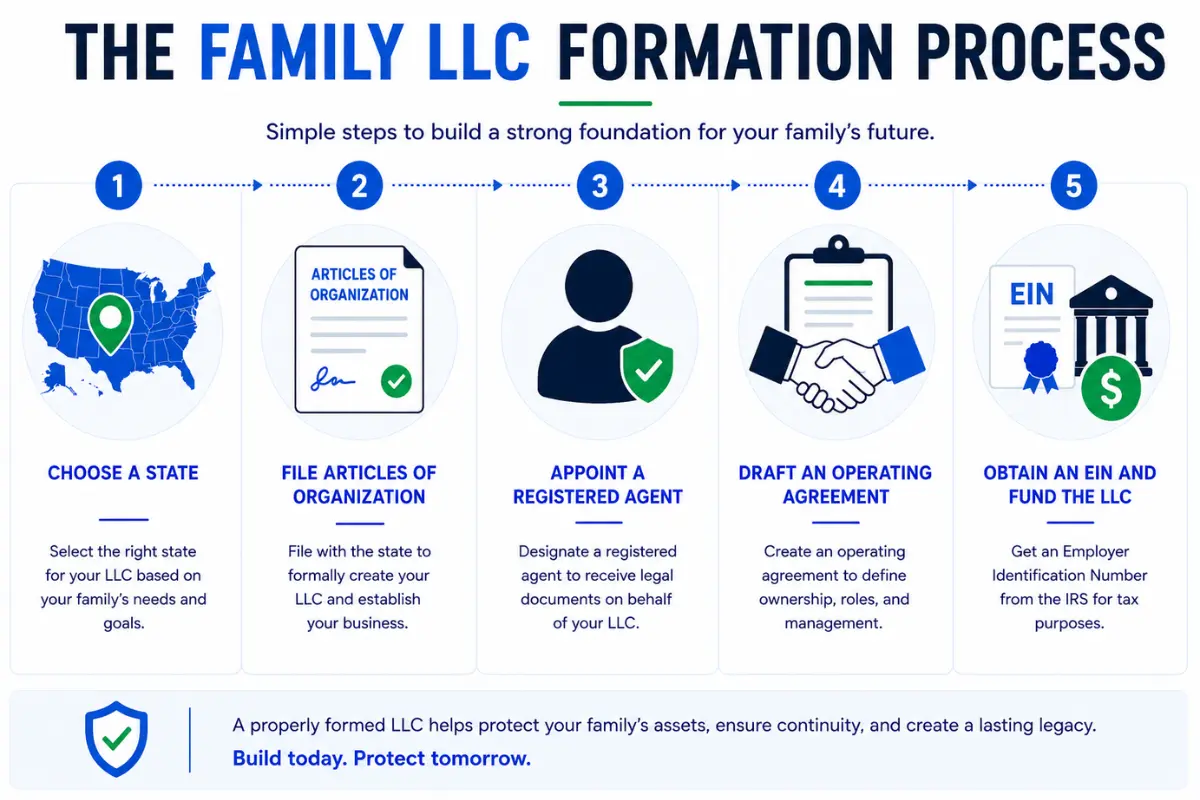

How to Form a Family Business LLC

The process of how to start a family LLC follows consistent steps across states, though specific requirements vary.

Step 1: Choose the State of Formation

Families typically form the LLC where the business operates. Some choose states with favorable LLC laws (Wyoming, Delaware) for privacy or asset-protection benefits, but this may require foreign registration in the home state, which adds cost.

Step 2: File Articles of Organization

The Articles of Organization are filed with the state's Secretary of State office to legally create the LLC. InCorp can assist with preparation and filing to ensure accuracy. Start your LLC formation with InCorp's streamlined process.

Step 3: Appoint a Registered Agent

Every LLC must designate a registered agent with a physical address in the state of formation to receive legal documents. A professional service like InCorp provides reliable availability, ensures compliance deadlines are met, and maintains privacy.

Step 4: Draft a Comprehensive Operating Agreement

The operating agreement is the most critical document for a family business LLC. It defines ownership, management authority, profit distribution, succession planning triggers, buy-sell agreement provisions, and dispute resolution. For family businesses, draft this with legal and tax professionals. Understanding whether you need an operating agreement helps families appreciate its importance.

Step 5: Obtain an EIN and Fund the LLC

Obtain a Federal Employer Identification Number from the IRS website for tax reporting and banking. Each family member should make their capital contributions as specified. Maintaining a separate business bank account is essential for preserving the liability shield.

Operating Agreement Essentials for a Family LLC

The operating agreement is the foundation of family governance. Without one, default state laws govern the business.

Ownership and Capital Contributions

The operating agreement should define each member's ownership percentage, initial capital contributions, and future contribution obligations. Ownership can reflect financial contributions, business roles, or estate-planning goals. For a multi-member LLC, clear documentation prevents disputes about contributions and establishes baselines for profit distribution calculations. A multi-member LLC structure requires particular attention to the definition of member rights and responsibilities.

Profit Distribution and Compensation

Specify how profits and losses are allocated and when distributions are made. LLCs can allocate profit distribution disproportionately to ownership if desired. Address compensation for active versus passive family members, benchmarking to market rates to avoid disputes and IRS scrutiny.

Voting Rights and Decision-Making

Define different decision-making levels: routine operational decisions, major decisions requiring majority vote, and fundamental decisions requiring unanimous consent. Creating different membership classes with varying voting rights allows founding members to transfer ownership while retaining control.

Buy-Sell Provisions

Buy-sell agreement provisions define what happens when a member leaves, retires, becomes disabled, divorces, or dies. Common elements include triggering events, valuation methodology, funding mechanisms (life insurance, installment payments), and right of first refusal.

Dispute Resolution

Include mandatory mediation or arbitration clauses to resolve disagreements without litigation. Having a predefined process helps prevent escalation and preserve family relationships.

Governance Structures for Family-Owned LLCs

Clear family governance separates successful family businesses from those struggling with conflict. Establishing effective family governance structures creates accountability and reduces potential for disputes.

Manager-Managed vs. Member-Managed

A manager-managed structure separates ownership from daily operations. Designated managers handle business decisions while other family members hold ownership without management authority. This management structure reduces conflict when some family members are active and others are not. Understanding single-member LLC vs multi-member LLC differences helps families structure ownership appropriately.

Family Council or Advisory Board

A family council meets regularly to discuss the direction of the business, progress on succession planning, and family concerns. Some families establish independent advisory boards composed of non-family members to provide objective guidance. This family governance mechanism separates family discussions from business operations.

Clear Role Definitions

Distinguish between family members who are owners only, owner-operators, and employees. The operating agreement should define each role's responsibilities, compensation, and authority to prevent confusion about roles.

Succession Planning in a Family LLC

Approximately 70% of family businesses lack a formal succession plan, explaining why so few survive beyond the second generation. Implementing family business succession planning strategies through the LLC structure addresses this critical challenge.

Start Planning Early

Begin succession planning 3-5 years before transition to identify and develop next-generation leaders and gradually transfer responsibilities. The operating agreement should define succession triggers such as retirement age, incapacity, or death.

Gradual Ownership Transfer

Gifting membership interests over time using the annual gift tax exclusion ($18,000 per recipient per year) reduces taxable estates while maintaining management control. Larger transfers can use the lifetime exemption ($13.61 million per individual, expected to decrease after 2025). Understanding how to transfer ownership of an LLC ensures proper execution.

Coordinating with Estate Plans

LLC succession planning should coordinate with each member's personal estate plan, including wills, trusts, and powers of attorney. Some families place LLC membership interests in revocable living trusts to avoid probate. These strategies require guidance from qualified professionals. Understanding business continuity planning helps families prepare for unexpected transitions.

Tax Advantages of a Family LLC

The family LLC tax advantages stem from pass-through treatment, valuation discounts, and strategic gifting.

Pass-Through Taxation

The LLC does not pay federal income tax. Business income passes through to each member's personal return based on ownership percentage, avoiding double taxation. This can result in significant tax savings, particularly with the Qualified Business Income deduction under Section 199A.

Valuation Discounts for Gift and Estate Tax

When transferring LLC membership interests, values may be discounted for gift and estate tax purposes. Two common valuation discounts: lack of marketability and minority interest. Combined discounts of 25% to 45% are common, significantly reducing tax burden on generational wealth transfers.

Annual Gifting Strategy

The annual gift tax exclusion allows each individual to gift up to $18,000 per recipient per year without triggering gift tax. For married couples gifting to multiple family members, this enables substantial ownership transfer with no tax consequences. The lifetime exemption ($13.61 million per individual in 2024) provides additional capacity but decreases after 2025. Understanding IRS gift tax rules helps families structure transfers appropriately.

Protecting the Business from Family Conflicts

Family dynamics create unique challenges. Proactive planning through the operating agreement helps prevent disagreements from threatening the business.

Prenuptial and Postnuptial Agreements

The operating agreement can restrict transfer of membership interests to non-family members, including spouses in divorce. Some families require prenuptial or postnuptial agreements as a membership condition to ensure ownership remains within the bloodline family.

Defined Exit Procedures

Clear procedures for when a member wants to leave protect both the exiting member and remaining owners. The buy-sell agreement provisions should define the valuation method, payment terms, and timeline.

Independent Advisors

Engaging independent advisors (attorneys, accountants, family business consultants) provides objective guidance and removes emotional decision-making from business operations. Research on avoiding traps that destroy family businesses provides valuable insights into common pitfalls.

Build Your Family Business LLC with InCorp

A family business LLC provides the legal framework for clear governance, orderly succession planning, asset protection, and tax-efficient generational wealth transfer. The family limited liability company structure combines operational flexibility with estate planning benefits that help families preserve their legacy across generations.

While forming the entity is a critical first step, maintaining it requires ongoing compliance, including annual report filings, registered agent service, proper record-keeping, and adherence to the operating agreement's provisions. Missing annual reports can result in administrative dissolution, losing the asset protection the LLC provides.

InCorp helps ensure that formation documents are prepared accurately, that registered agent requirements are met in every state where you operate, and that compliance deadlines are tracked through our EntityWatch® system. Whether you're forming your first family LLC for asset protection or restructuring an existing family LLC for estate planning, InCorp provides the professional support families need to establish and maintain effective governance and protection structures.

Start your LLC formation with InCorp today and build the legal foundation your family business deserves.

FAQ's

What is a family LLC?

A family LLC is a limited liability company whose members are related by blood, marriage, or adoption. It functions like any other LLC but is specifically structured to hold and manage family assets or a family business. The operating agreement defines each member's ownership interest, management authority, profit distribution, and succession planning procedures. Family LLCs are commonly used for operating businesses, real estate holdings, investment management, and estate planning.

What is the difference between a family LLC and a family trust?

A family business LLC is a business entity that provides asset protection, flexibility in management structure, and pass-through taxation. A family trust is an estate planning vehicle designed to hold and distribute assets according to the grantor's wishes, often to avoid probate. Some families use both structures together, placing LLC membership interests inside a trust for estate planning purposes. The right approach depends on the family's goals, and consulting with an estate planning attorney is recommended to evaluate family LLC vs family trust options.

Can a family LLC help reduce estate taxes?

A family LLC for estate planning can be part of an estate tax reduction strategy. When membership interests are transferred to family members, the value of those interests may qualify for valuation discounts (lack of marketability and minority interest), which can reduce the gift and estate tax burden. Combined discounts of 25% to 45% are common. These strategies require careful planning with qualified tax and legal professionals to ensure proper documentation and compliance.

What should be included in a family LLC operating agreement?

A comprehensive family LLC operating agreement should address ownership percentages, capital contributions, profit distribution, voting rights and decision-making thresholds, management structure (manager-managed vs. member-managed), buy-sell agreement provisions, succession triggers, dispute resolution procedures, restrictions on transfer of membership interests, and procedures for admitting or removing members. For family businesses, it is also advisable to address compensation policies, employment prerequisites, and divorce-related transfer restrictions.

What happens if a family member wants to leave the LLC?

The operating agreement should include buy-sell agreement provisions that define the process for a member's voluntary withdrawal. These typically include a right of first refusal for remaining members, a defined valuation methodology, and payment terms. Common funding mechanisms include life insurance, installment payments, or a sinking fund. Without these provisions, default state laws govern the process, which may not reflect the family's preferences and can lead to disputes over valuation and payment terms.

How can family business owners involve non‑active family members in succession planning without disrupting daily operations?

Family business owners can invite non‑active family members into structured forums such as a family council or periodic family meetings focused on long‑term vision, ownership succession, and family values, rather than day‑to‑day business decisions. This keeps them informed and respected as owners while leaving business leadership and operational decision making to active family members or professional management, which supports both family harmony and business continuity.

What role do professional advisors play in a family business succession planning process?

Professional advisors such as estate planning attorneys, tax professionals, and financial advisors help design legal structures, ownership transfer strategies, and estate plans that align with the family's goals and minimize estate taxes where possible. They can also serve as neutral voices during the succession planning process, helping family business owners evaluate practical strategies, draft buy‑sell agreements, and build governance structures that support a smooth transition to future generations.

How can a family council support strong governance in a family-owned business LLC?

A family council provides a regular forum for key family members to discuss shared goals, family values, and long‑term business direction separately from operational meetings. It can help identify potential successors, review the succession plan, and address family communication issues early, which reduces the risk of family conflict spilling over into business decisions and supports a more successful business transition.

Why is a buy-sell agreement important for a family business LLC's succession plan?

A buy‑sell agreement sets clear rules for what happens if a family member owner dies, becomes disabled, retires, or wants to exit, including how their ownership interest will be valued and who can buy it. Having these terms agreed upon in advance helps avoid disputes among family members, supports financial security for the departing owner or their heirs, and protects the business from sudden ownership changes that could threaten business performance or continuity.

How can family business owners prepare the next generation for leadership transition?

Owners can create a formal development plan for potential successors that includes education, rotational roles in different parts of the family enterprise, mentoring from current leaders, and clear performance expectations. Combining on‑the‑job experience with leadership training and regular feedback helps ensure that when a key leader eventually steps down, the next generation is prepared to assume business leadership in a way that supports long‑term success and the family legacy.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.