Business Scaling Strategies: How to Expand Your LLC From Solo to Team

Many business owners hit a moment where the work coming in finally outpaces what one person can keep up with. A consultant turning down referrals, a contractor stretching weekend hours into Monday, or an online seller losing track of fulfillment all point to the same thing: demand has run ahead of capacity. Business scaling is the response to that moment, and it usually requires more than another set of hands. The transition from a single-member LLC to a team-based business involves legal, tax, and structural decisions that shape what the company can become.

Approximately 85.8% of U.S. small businesses operate without a single employee, which is a useful reminder that going solo is normal rather than a stalling point. The owners who do scale tend to plan the move rather than improvise it. Effective business scaling is not just hiring help. It means updating the LLC's legal structure, maintaining compliance as new tax obligations attach, and building repeatable systems that can carry growth without breaking under it. Owners working through that transition often lean on an administrative partner like InCorp to keep the formation, compliance, and registered agent pieces current as the business changes shape.

What follows covers when a solo LLC is ready to grow, contractors versus employees for a first hire, hiring through an LLC, converting to a multi-member structure, updating the operating agreement, and the tax implications of building a team.

Key Takeaways

-

Scaling from a solo to a team‑based LLC is less about headcount and more about timing: consistent demand, repeatable processes, and clear revenue potential are key signs your business is ready to grow.

-

Choosing between contractors and employees for your first hire has major compliance and tax implications, and misclassifying workers can trigger IRS scrutiny, back payroll taxes, and state‑level penalties.

-

Hiring employees through an LLC requires an EIN, state labor and tax registrations, payroll withholding, and documented onboarding so you stay compliant with federal and state employment rules from day one.

-

Converting from a single‑member to a multi‑member LLC changes ownership, tax filings, and decision‑making, and usually calls for updating the operating agreement and state records to reflect the new structure.

-

As your LLC scales, maintaining clean books, honoring the operating agreement, and staying current on state compliance is what preserves your liability shield and keeps growth from creating hidden legal risk

Signs Your Solo LLC Is Ready to Scale

Effective business scaling starts with recognizing when the timing is right. Going solo is normal for most small businesses, but for owners experiencing consistent demand, staying solo can quietly cap the upside. The same benefits of forming an LLC, including liability protection, pass-through taxation, and operational flexibility, apply at any size, but the way the business structure is run has to change as headcount grows.

Consistent Revenue and Demand

The clearest indicator is sustained revenue that exceeds what one person can deliver. When the business is consistently turning away work, missing deadlines, or unable to take on new clients, the bottleneck has shifted from finding business to fulfilling it. A useful financial guardrail is having three to six months of payroll reserves before hiring, which covers the gap between paying a new team member and the productivity gains showing up on the books.

Repeatable Processes

Before bringing on team members, the business should have documented, repeatable processes for the work being delegated. Tasks that can be clearly defined, taught in a few sittings, and checked against a predictable output are the strongest candidates for a first hire. Without documented systems, the onboarding process becomes inefficient and quality control may suffer.

Revenue Growth Potential

Small businesses with one to four employees generate an average of $387,000 in annual revenue, while those with 10 to 19 employees bring in approximately $2.16 million, according to recent small business revenue benchmarks. The jump is not a guarantee, but it illustrates the math behind why owners scale at all. The reverse is also true. Adding people without the systems or demand to support them turns a hiring decision into an overhead problem.

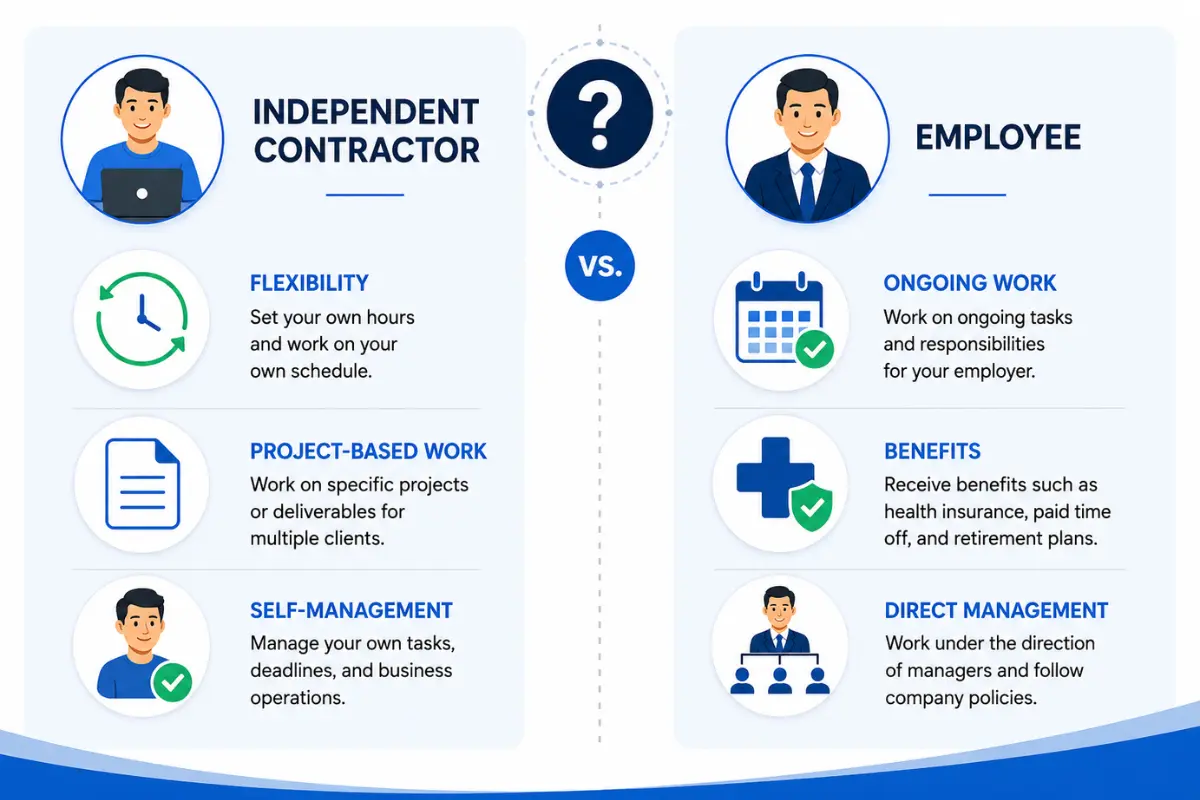

Contractors vs Employees: Choosing Your First Hire

Once an LLC is ready to grow, the next decision is what kind of help to bring in. Independent contractors and employees are both legitimate options, but the legal, tax, and operational implications run in opposite directions. Picking the wrong category can trigger IRS reclassification, back taxes, and liability that the LLC's business structure was supposed to keep at arm's length.

When to Use Independent Contractors

An independent contractor is typically best suited for project-based or specialized work that does not require daily oversight. Contractors set their own schedules, use their own tools, and are responsible for their own taxes, which means the LLC does not withhold income tax, pay the employer portion of payroll taxes, or carry workers compensation coverage. The IRS uses specific behavioral, financial, and relationship criteria to determine whether a worker is genuinely independent. Treating an independent contractor like an employee, by assigning fixed hours or supplying tools, can invite reclassification, back payroll taxes, and state-level penalties.

When to Hire Employees

Employees become the better fit when the work is ongoing, requires direct supervision, and is central to the business's core operations. The cost is real: the LLC must obtain an employer identification number, set up payroll withholding, register with state labor and tax agencies, and provide required benefits such as workers compensation and unemployment insurance. The SBA's guide to hiring a first employee lays out the federal baseline. According to the Federal Reserve's 2025 Small Business Credit Survey, 57% of small businesses plan to hire in 2026, while 46% report challenges finding and retaining workers.

The Hybrid Approach

Many scaling LLCs start with independent contractors during uncertain growth phases, then convert to employees once demand stabilizes. Contractors let the business test whether additional capacity is truly needed before committing to the full compliance requirements of employment. The hybrid path works best when the contractor relationship is genuinely arm's-length from the start, since transitioning a contractor in name only to W-2 status can flag the original arrangement as misclassification.

How to Hire Your First Employee Through an LLC

A single-member LLC can hire an unlimited number of employees. The LLC structure does not restrict team size. The obligations of being an employer attach once the first W-2 worker is hired, whether the LLC has one member or fifty employees on payroll. The four steps below cover the federal and state baseline, with the caveat that specific state requirements vary.

Step 1: Obtain an Employer Identification Number (EIN)

If the LLC does not already have an employer identification number, the owner has to apply for one through the IRS before payroll can run. The EIN is the federal tax ID used for payroll tax reporting, opening a business bank account, and filing employment-related tax forms. Single-member LLCs without employees often use the owner's Social Security number, but hiring a first employee triggers the EIN requirement. The application is free directly through the IRS EIN application.

Step 2: Register With State and Local Agencies

Once the EIN is in hand, the LLC has to register with the state's labor and tax agencies for unemployment insurance, workers compensation, and state income tax withholding. Compliance requirements vary enough that an out-of-state owner can easily miss a filing window, with some states adding registrations for paid family leave or city-level wage taxes. Confirming obligations through the state's state business licensing resources before the first paycheck goes out keeps the business from picking up penalties on day one. The registered agent on file is the address where the state delivers legal notices, and many owners hand off the role to a professional registered agent service.

Step 3: Set Up Payroll and Tax Withholding

Each new employee completes IRS Form W-4 for federal tax withholding and Form I-9 for employment eligibility verification before the first paycheck runs. The employer withholds federal income tax, the employee's share of Social Security and Medicare taxes (7.65% of wages), and applicable state and local taxes, plus a matching 7.65% as the employer share. Most small businesses use payroll software or a payroll service to manage the calculations and quarterly filings, since the IRS treats unpaid payroll taxes as a high-priority enforcement area.

Step 4: Establish Employment Policies and Onboarding

As the business brings on team members, clear job descriptions, written employment agreements, and a defined onboarding process help set expectations on both sides. The IRS requires employers to keep records of employment taxes for at least four years, and most states impose their own retention rules. A repeatable onboarding process built around tax forms, role expectations, and the LLC's basic policies gets each new hire past day one without making the first week feel improvised.

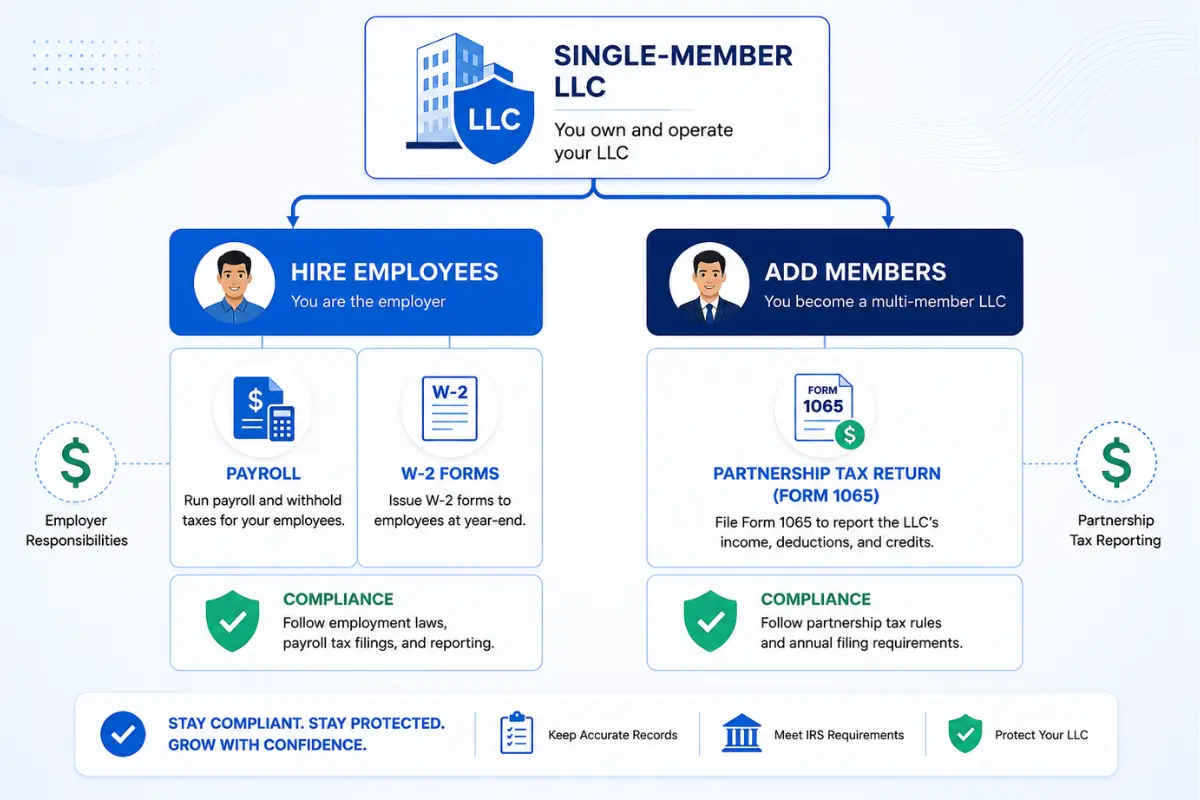

Converting From Single-Member to Multi-Member LLC

Not every scaling decision involves hiring W-2 employees. Some LLC owners scale by bringing in partners, co-owners, or investors as members of the entity itself, which converts a single-member LLC into a multi-member LLC. The shift changes how the IRS classifies the entity, how income is reported, and how decisions are made internally, and it usually means rewriting the operating agreement to match the new ownership reality.

When Conversion Makes Sense

Conversion to a multi-member structure tends to come up when the owner wants to share ownership intentionally, take on capital from a partner, or formalize a co-founder relationship that was running on a handshake. Adding a member also changes the LLC's default tax classification from a disregarded entity to a partnership, which has significant implications for how income is reported. Conversion is also difficult to reverse: returning to a single-member LLC after adding members usually requires buying out the additional member, which carries its own legal and tax complications.

Steps to Convert

The conversion process generally follows a familiar arc: amend the existing operating agreement to reflect the new ownership, file an amendment to the articles of organization with the state if the public record changes, obtain a new employer identification number from the IRS, update the business bank account, and revise any business licenses or permits that list ownership information. A new EIN is specifically required when the LLC's tax classification changes from a disregarded entity to a partnership, even if the LLC has had an EIN since business formation. Most jurisdictions treat ownership changes as amendable rather than triggering a brand-new entity, which keeps the LLC's history, contracts, and licensing intact.

Management Structure Decisions

A multi-member LLC has to decide between a member-managed and a manager-managed business structure. In a member-managed LLC, every member participates in daily operations, which fits small partnerships where members are also the operators. In a manager-managed LLC, the members appoint one or more managers to handle day-to-day decisions, which fits when some members are passive investors. The InCorp guide on single-member vs multi-member LLC covers the broader differences in tax treatment and governance, and the Asena Advisors guide to LLC conversion walks through the practical filing sequence.

Updating Your Operating Agreement for Growth

The operating agreement is the internal document that tells members and the outside world how the LLC is supposed to run, and it pairs with the articles of organization on file with the state to define how the entity operates. The version drafted at business formation is rarely the right document for a multi-member LLC with a growing team and registered agent notices arriving from multiple states.

Key Provisions to Update

Several provisions in the operating agreement tend to need revision once the LLC scales:

-

Ownership percentages and capital contributions

-

How profits and losses are allocated and distributed

-

Voting rights and decision-making procedures

-

Roles and responsibilities of each member or manager

-

Procedures for adding or removing members

-

Buyout and exit provisions

-

Dispute resolution mechanisms

If the ownership change touches the public record, the articles of organization may also need a corresponding amendment with the state. Even in states that do not legally require a written operating agreement, having one is critical for maintaining the LLC's liability protection. The SCORE guide to operating agreement provisions covers the standard provisions.

Protecting the Liability Shield

As the LLC grows, maintaining the separation between personal and business affairs becomes more important, not less. Commingling funds, ignoring the operating agreement, or skipping state compliance requirements can lead to a court "piercing the corporate veil" and holding the owners personally liable for business debts. Regular reviews of the operating agreement and clean state compliance habits keep the liability protection the LLC structure offers from quietly eroding.

Tax Implications of Scaling Your LLC

Scaling an LLC changes the entity's tax obligations. Hiring employees adds payroll tax responsibilities, adding members changes how the LLC is taxed at the entity level, and either move can shift state tax exposure depending on where the business operates.

Payroll Tax Obligations for Employers

Once an LLC hires employees, it becomes responsible for payroll taxes on top of wages. The employer share covers Social Security and Medicare (7.65% of wages), federal unemployment tax, and state unemployment tax, plus the employer is responsible for withholding the employee share of Social Security, Medicare, and federal income tax. Total employment costs typically add 25 to 40% to base wages once payroll taxes, insurance, and benefits are factored in. Employers must also file quarterly payroll tax returns (Form 941) and annual W-2 wage reports.

Tax Changes When Adding Members

A single-member LLC is treated as a disregarded entity for federal tax purposes by default, a form of pass-through taxation where business income flows directly to the owner's personal return. Adding a second member changes the default to partnership taxation, which keeps the pass-through taxation structure but requires the LLC to file Form 1065 annually and issue a Schedule K-1 to each member. The LLC can also elect S-corporation tax treatment by filing Form 2553, which can reduce self-employment tax for qualifying businesses. The Ventures Smarter guide to adding an employee walks through the tradeoffs.

State Tax Considerations

Some states layer additional taxes onto LLCs that grow past a certain size: franchise taxes, gross receipts taxes, or higher annual fees that scale with revenue or member count. California, Tennessee, and Texas are common examples. State tax exposure also expands as the business hires employees in additional states, since each state where wages are paid generally creates a filing obligation. The InCorp page on comparing entity types covers the structural tax differences across LLC, S-corp, and C-corp options.

Scale Your LLC With Confidence Through InCorp

Business scaling from a solo LLC to a team-based operation is a sequence of related decisions: when to add capacity, what kind of help to bring in, how to handle the legal and tax obligations, and how to keep the business structure aligned with the business as it grows. Compliance is what carries the rest. Annual report filings, registered agent coverage, EIN updates, and accurate employment records decide whether the LLC stays in good standing or quietly drifts out of it, and consistent compliance is what keeps the LLC's liability protection intact through every transition.

InCorp's LLC formation services and EntityWatch® compliance system handle business formation amendments, registered agent representation in all 50 states, and ongoing compliance tracking so owners can focus on running the business.

FAQ's

Can a single-member LLC hire employees?

Yes, a single-member LLC can hire an unlimited number of employees. The LLC must first obtain an employer identification number, register with state labor and tax agencies, set up payroll withholding, and obtain workers compensation insurance. Hiring employees does not change the LLC's single-member classification.

What is the difference between hiring an employee and adding a member to an LLC?

Employees work for the LLC in exchange for wages and hold no ownership interest. Members are owners who share in profits, losses, and management according to the operating agreement. Hiring an employee does not change the ownership structure, while adding a member converts the LLC from single-member to multi-member and changes tax filings, liability exposure, and decision-making authority.

Do I need a new EIN when I add a member to my LLC?

In most cases, yes. When a single-member LLC adds a member and changes its tax classification from a disregarded entity to a partnership, the IRS requires a new employer identification number. The application can be completed online through the IRS website at no cost.

Should I hire contractors or employees when scaling my LLC?

The decision depends on the nature of the work and the level of control needed. Independent contractors fit project-based, specialized work where the worker controls how and when it is completed. Employees are typically appropriate for ongoing work that requires direct supervision. The IRS uses specific behavioral, financial, and relationship criteria to classify workers, and misclassifying employees as independent contractors can result in penalties and back taxes.

What compliance requirements change when my LLC hires its first employee?

Hiring a first employee triggers several new compliance requirements: obtain an EIN, register with state labor and unemployment agencies, set up payroll tax withholding, purchase workers compensation insurance, verify employment eligibility using Form I-9, and maintain employment tax records for at least four years. Some states require additional registrations for disability insurance or paid family leave.

How can a solo service-based business owner decide when it is the right time to make a first hire?

The timing is usually right when you have consistent work, repeat business from existing clients, and a steady flow of qualified leads that your current capacity cannot fully serve. If you are turning down projects, working unsustainable hours, or seeing cash flow issues because you cannot invoice promptly or deliver on time, it is a sign that adding team members could support sustainable growth rather than just more busyness.

What roles are best suited for a first hire in a growing service-based company?

For many solo entrepreneurs, the first team member is someone who can take over repetitive admin tasks, client communication follow-ups, or routine project management so the owner can focus on revenue-generating work. In other businesses, a virtual assistant or operations coordinator who can help with client onboarding, scheduling, and basic customer relationship management provides the biggest lift without compromising quality.

How can small business owners scale operations without compromising quality or customer experience?

The key is to build standard operating procedures for core service delivery and client communication before or alongside hiring, so new employees can follow a clear blueprint. Using the right tools for project management, CRM, and collaboration helps small teams maintain consistent client experience and service quality even as they take on more customers and more complex work.

When does outsourcing non-core functions make sense for scaling your business?

Outsourcing non-core functions such as bookkeeping, basic marketing execution, or IT support can free the business owner and first team members to focus on service delivery and business growth. It is particularly helpful when cash flow can support the cost, but the business is not yet large enough to justify full-time hires in those areas, and when external specialists can perform those tasks more efficiently.

What mindset shift do business owners need to make when moving from solo business to leading a team?

Scaling from solo to team requires shifting from "I do everything myself" to "I design systems and lead people," which means investing time in leadership development and communication rather than just client work. Business owners have to view hiring and training as long-term investments in a scalable business model, aligning roles, tools, and processes with their growth goals and long-term success.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.