Choosing the Right Structure for Your Real Estate Business

A real estate investor purchased three rental properties over five years, holding all titles in his personal name. When a tenant's lawsuit from a property incident exposed all assets, including his home and retirement accounts, the lack of proper real estate business structuring transformed a property-specific problem into a wealth-threatening catastrophe.

The primary goal of real estate business formation is to protect personal assets from property-related liabilities while optimizing tax efficiency. There are an estimated 19.3 million rental properties in the U.S., with 15.4% held by LLCs and LLPs and 70.2% owned by individuals, according to Indestata. The three main vehicles include the LLC, Corporation, and Trust, each serving distinct strategic purposes for different real estate business models.

While LLCs and Corporations are business entities formed through state filings, a Trust is a legal arrangement that requires the expertise of an attorney. There were about 3,758,070 real estate and rental businesses in the U.S. in 2025, according to IBISWorld. Understanding the best entity for real estate investing requires evaluating liability protection, tax treatment, and wealth transfer objectives.

Key Takeaways

-

The core job of your structure is to separate your personal assets from property-related risks while still giving you tax efficiency and financing flexibility.

-

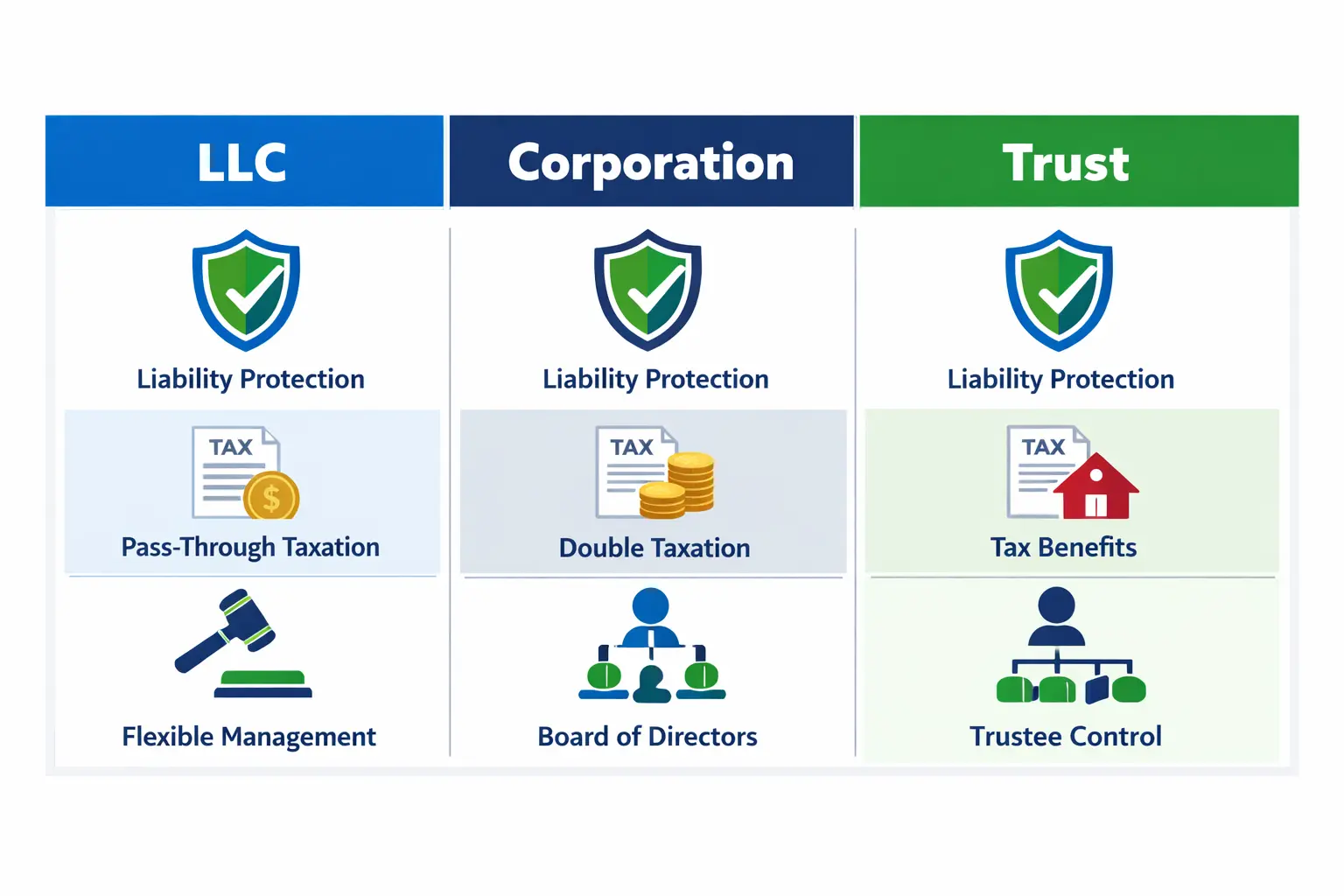

LLCs are the default choice for many real estate investors because they combine limited liability protection, pass‑through taxation, and relatively simple ongoing compliance compared with corporations.

-

Corporations (C‑corps and S‑corps) can make sense for large, high‑volume or active operations—like development or property management—but often add complexity and can trigger double taxation if not used carefully.

-

Trusts are best viewed as estate‑planning and privacy tools, often layered on top of LLCs or corporations to handle probate avoidance, succession, and confidentiality rather than day‑to‑day business operations.

-

Many experienced investors use a hybrid approach, such as a holding LLC with separate property LLCs or LLC interests owned by a trust, to combine asset protection, tax planning, and long‑term wealth transfer in one integrated strategy.

The Limited Liability Company (LLC): The Investor's Standard

The LLC represents the most common choice for real estate investors due to its blend of liability protection and administrative simplicity. Real estate LLC formation creates a corporate shield separating investors' personal wealth from property-related lawsuits or debts. The limited liability protection prevents creditors from pursuing personal assets, such as homes, savings accounts, or investment portfolios, to satisfy business debts or legal judgments.

Forming an LLC requires filing Articles of Organization with the state and paying applicable filing fees. Most states require Operating Agreements documenting ownership percentages, profit distribution methods, and management procedures. The single-member LLC for rental property provides the same protection as multi-member LLCs with simplified reporting and operational flexibility for solo investors.

Pass-Through Taxation Benefits

By default, the IRS treats LLCs as pass-through entities, allowing profits and losses to flow directly to members' personal tax returns without corporate-level taxation. This avoids double taxation, in which profits are taxed at the corporate and shareholder levels. Depreciation deductions for real estate pass through to LLC members, providing significant tax benefits offsetting rental income.

Pass-through taxation allows deducting property expenses, mortgage interest, taxes, insurance, and depreciation on personal returns. This tax treatment proves particularly advantageous for investors holding multiple rental properties, as losses from one property can offset gains from others. The single-member LLC for rental property receives pass-through treatment by default, with rental income reported on Schedule E.

Operational Flexibility

LLCs have fewer formal requirements than corporations, eliminating the need for boards of directors or mandatory annual meetings. This simplified structure reduces administrative burden while maintaining legal protection. Investors can hold multiple properties in separate LLCs to isolate risks, preventing problems at one property from endangering other holdings.

The Series LLC structure in certain states allows the creation of multiple protected series under one parent LLC, with each series holding different properties and maintaining separate liability protection. This reduces formation costs while providing risk isolation benefits. Investors managing diverse portfolios benefit from operational flexibility, allowing different management structures for different property types.

The Corporation (Corp): Scalability for High-Volume Ventures

The Corporation functions as a formal legal entity suitable for large-scale real estate operations or for entities seeking to raise capital through stock issuance. The real estate corporation structure offers robust liability protection through the corporate veil, separating shareholders from corporate debts and liabilities. While providing strong protection, corporations carry higher administrative burdens and more complex tax rules than LLCs.

Corporate formalities include maintaining boards of directors, holding annual meetings, recording minutes of major decisions, and issuing stock certificates. These requirements, while burdensome, strengthen the corporate veil protecting shareholders. Understanding the differences between selling corporations versus LLCs helps investors plan exit strategies and assess the structural implications for future transactions.

C-Corp vs. S-Corp for Real Estate

C-Corporations face double taxation, in which profits are taxed at both the corporate and shareholder levels. However, C-Corps benefit entities that reinvest profits rather than distribute them, as retained earnings fund acquisitions without triggering shareholder taxation. The C-Corp structure suits real estate developers and large-scale operators planning significant capital reinvestment.

S-Corp election allows LLCs or Corporations to elect special tax treatment, reducing self-employment taxes, provided IRS requirements are met. S-Corp status requires reasonable compensation through payroll, with remaining profits distributed as dividends, avoiding self-employment tax. This structure benefits active real estate professionals generating substantial income from property management or development activities.

Enhanced Governance and Capital Raising

Formal corporate structures with bylaws and board oversight provide a stronger defense against a corporate veil piercing when properly maintained. Courts scrutinize whether corporations observe required formalities when determining shareholder liability. Detailed documentation, separate finances, and consistent compliance with corporate procedures strengthen liability protection.

Corporations represent the preferred vehicle for investors planning to issue shares to stockholders or raise significant capital. Different stock classes accommodate various investor types and structures. Real estate investment trusts (REITs) and large development companies typically operate as corporations due to the capital-raising advantages of corporate structures.

The Real Estate Trust: Privacy and Estate Planning

A Trust is a fiduciary arrangement in which a trustee holds legal title to property for the beneficiaries' benefit. Trusts are not business entities like LLCs or corporations and typically require the expertise of an attorney for proper implementation. The fiduciary duty requires trustees to manage assets solely for the beneficiaries' benefit, creating legal obligations that exceed those governing corporate directors or LLC managers.

Trusts focus primarily on estate planning, privacy protection, and wealth transfer rather than operational business management. Real estate investors use trusts alongside business entities to implement comprehensive asset protection and estate planning strategies. The Trust structure provides benefits unavailable through business entities alone, particularly regarding probate avoidance and privacy protection.

Asset Transfer and Probate Avoidance

Trusts transfer assets to beneficiaries outside of probate, which can take months or years depending on the estate's complexity. Property title transfer through Trust provisions occurs automatically upon death, ensuring continuity of management for real estate assets. This immediate transfer prevents disruption to rental income and maintains property management during ownership transitions.

Probate avoidance saves beneficiaries substantial legal fees, court costs, and delays. Properties held in Trusts remain private, avoiding public disclosure required in probate. The seamless transfer particularly benefits real estate portfolios, where management continuity ensures the continuity of rental operations.

Anonymity and Privacy Protection

Land Trusts or Privacy Trusts allow investors to keep names off public property records, adding security against scrutiny and frivolous lawsuits. Public records typically disclose property ownership, potentially exposing investors to targeted legal actions or revealing investment strategies to competitors. Trust ownership obscures beneficial owners' identities while maintaining clarity of legal title for financing and transaction purposes.

Privacy protection proves particularly valuable for high-net-worth individuals, public figures, or investors managing portfolios across multiple jurisdictions. Understanding differences between privacy, security, and anonymity helps investors implement protective measures. However, privacy benefits must be balanced against lender requirements and regulatory disclosure obligations affecting Trust-held properties.

Comparative Analysis: Liability, Taxes, and Governance

The real estate business structure comparison reveals the strengths of each option, addressing specific investor needs and risk profiles. Direct comparison helps investors identify best fits for goals and strategies. Evaluating liability protection, tax treatment, and operational requirements provides a framework for informed structure selection.

Liability Comparison

Statutory liability protection of LLCs and Corporations provides stronger shields against business liabilities than contract-based Trust protections. LLCs and Corporations create separate legal entities, with creditors limited to entity assets. Investors should also consider protecting intellectual property through patents, copyrights, and trademarks when building real estate brands.

Irrevocable Trusts offer stronger asset protection than revocable Trusts because grantors relinquish ownership and control over Trust assets. This separation generally makes Trust assets unavailable to grantor creditors, though specific state laws and Trust provisions affect the level of protection. Combining entity liability protection with Trust asset protection creates comprehensive defensive strategies addressing multiple risk categories.

Tax Treatment Summary

Pass-through taxation of LLCs allows profits to flow to members' personal returns, avoiding corporate taxation. This benefits real estate investors utilizing depreciation deductions, offsetting personal income. C-Corporations face double taxation on distributed profits, whereas retained earnings avoid shareholder-level taxation until distributed.

Revocable Trusts provide no independent tax benefits, with Trust income taxed on the grantor's personal returns. Irrevocable Trusts function as separate tax entities filing independent returns. The S-Corp election provides tax benefits for active real estate professionals through self-employment tax savings.

Strategic Combination: The "Parent-Subsidiary" Approach

Sophisticated investors combine structures to maximize benefit, creating layered protection that addresses different risk categories. Having LLCs hold property titles while Trusts own LLC interests represents a common hybrid approach. This parent-subsidiary model combines an LLC's operational flexibility with the security and privacy benefits of a Trust.

The combination of LLCs within Trusts provides comprehensive strategies protecting against both operational liabilities and estate planning challenges. The LLC protects against property-related lawsuits while the Trust shields ownership from probate and maintains privacy. This dual-layer approach addresses immediate liability concerns and long-term wealth transfer objectives simultaneously.

Key Considerations Before Choosing a Structure

Investors should consider exit strategies, financing needs, and the number of partners before finalizing structures. Lenders often have different requirements for LLC-owned versus personally owned properties, which can affect loan qualification. Some lenders require personal guarantees regardless of entity structure.

The state of formation impacts protection levels and compliance costs. States like Delaware, Nevada, and Wyoming offer strong LLC statutes. Annual state filing requirements and franchise taxes vary dramatically by jurisdiction. Asset protection for real estate investors is strengthened through proper documentation, separate finances, and consistent compliance with entity formalities.

The Role of Professional Compliance and Maintenance

Maintaining Good Standing with the state is essential to preserving liability protection, regardless of the structure chosen. Administrative dissolution due to missed filings or unpaid fees eliminates the entity's protection, exposing personal assets to business liabilities. The registered agent requirement ensures entities receive legal and tax notices promptly, preventing missed deadlines and causing compliance problems.

Failing to file annual reports or pay franchise taxes triggers administrative dissolution, potentially piercing the corporate veil and eliminating liability protection. Understanding Certificate of Good Standing requirements helps maintain compliance across all jurisdictions. Professional registered agent services provide reliable notice receipt, privacy protection, and compliance monitoring, preventing missed deadlines.

Professional Formation and Monitoring Services

Professional filing services ensure LLCs and Corporations are formed accurately with proper documentation. While InCorp does not form Trusts, they provide specialized support for business entity formation. The EntityWatch® system helps owners monitor standing and filing deadlines across all states.

Final Thoughts

While LLCs and Corporations provide robust foundations for real estate business ventures, Trusts serve as powerful tools for estate management and privacy. The optimal structure depends on specific goals and objectives.

Explore InCorp's LLC and Corporation formation services to help establish your real estate business on a solid legal footing. The EntityWatch® system monitors state requirements and maintains compliance necessary for investment success.

Visit InCorp's business services to discover comprehensive solutions supporting real estate business formation, compliance, and growth.

FAQ's

Can I change my real estate business structure later if my strategy evolves?

Yes. Many investors start with one structure and later convert or layer entities as their portfolio or needs change. Conversions may trigger tax consequences or require a property title transfer, so professional guidance helps ensure a smooth transition.

Do lenders treat entity-owned real estate differently from personally owned property?

Often, yes. Some lenders apply stricter underwriting standards or require personal guarantees when property is held in an entity. The personal guarantee can eliminate liability protection benefits for that specific debt.

Is one entity required for every property I own?

No. While some investors treat each property as a separate entity for maximum liability protection, others group multiple properties based on risk tolerance and administrative capacity. The optimal approach balances risk isolation against operational efficiency.

Does forming a business entity automatically provide insurance coverage?

No. Legal structures limit liability exposure, but adequate property and umbrella insurance remain necessary for comprehensive risk management. Combining proper entity structure with appropriate insurance creates layered protection.

How does an LLC help real estate investors protect personal assets?

A limited liability company creates a separate legal entity so that rental properties and other real estate holdings are owned by the LLC rather than by you personally. If the rental business faces a lawsuit or unpaid debt and you've kept personal and business finances separate, liability protection generally limits creditors to business assets inside the LLC instead of your home, personal savings, or other non‑business property.

When might an S corporation election make sense for a real estate business?

For many buy‑and‑hold rental properties, an LLC taxed as a simple pass through entity is often sufficient, because rental income is usually not subject to self employment tax. An S corporation election may be more appropriate for active real estate businesses—such as property management companies or real estate service firms—where the owner takes a reasonable salary and then distributes extra profits, potentially reducing self employment tax on part of the income.

Is a sole proprietorship ever the right structure for real estate investing?

A sole proprietorship can be a starting point for a very small, low‑risk real estate business, such as a single short‑term rental or side‑gig management activity held in your own name. However, because there is no personal liability protection and business debts or lawsuits can reach personal assets, many real estate investors move to a formal business structure like an LLC once they own multiple properties or have significant personal assets to protect.

How should real estate investors handle bank accounts and expenses under different structures?

Regardless of whether you choose a single member LLC, multi member LLC, or corporation, you should maintain a dedicated business bank account for rental income and business expenses. Keeping business funds and personal finances separate helps preserve liability protection, simplifies tax treatment, and provides clearer records if questions arise about whether your entity truly operates as a distinct business.

What factors should I consider when choosing the most tax‑efficient structure for my real estate portfolio?

Key questions include whether your income comes mainly from passive rental income or active real estate businesses, how many properties you hold, whether you plan to raise capital, and your tolerance for administrative complexity. Many real estate investors use pass through taxation via LLCs for rental properties to avoid entity level tax and double taxation, and may layer in S corp or C corp structures for active service businesses, often with professional guidance to balance tax savings against compliance costs.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.