Types of Business Entities: What Business Owners Need to Know Before Forming

An entrepreneur spent weeks researching Types of Business Entities online, finding conflicting advice about which structure would "save the most taxes" or provide "complete protection." She formed an LLC based on a forum recommendation, only to discover later that her specific business activities and growth plans made a corporation more suitable. The conversion process created unexpected tax consequences and delayed her funding round. Understanding entity characteristics before formation helps avoid such costly restructuring.

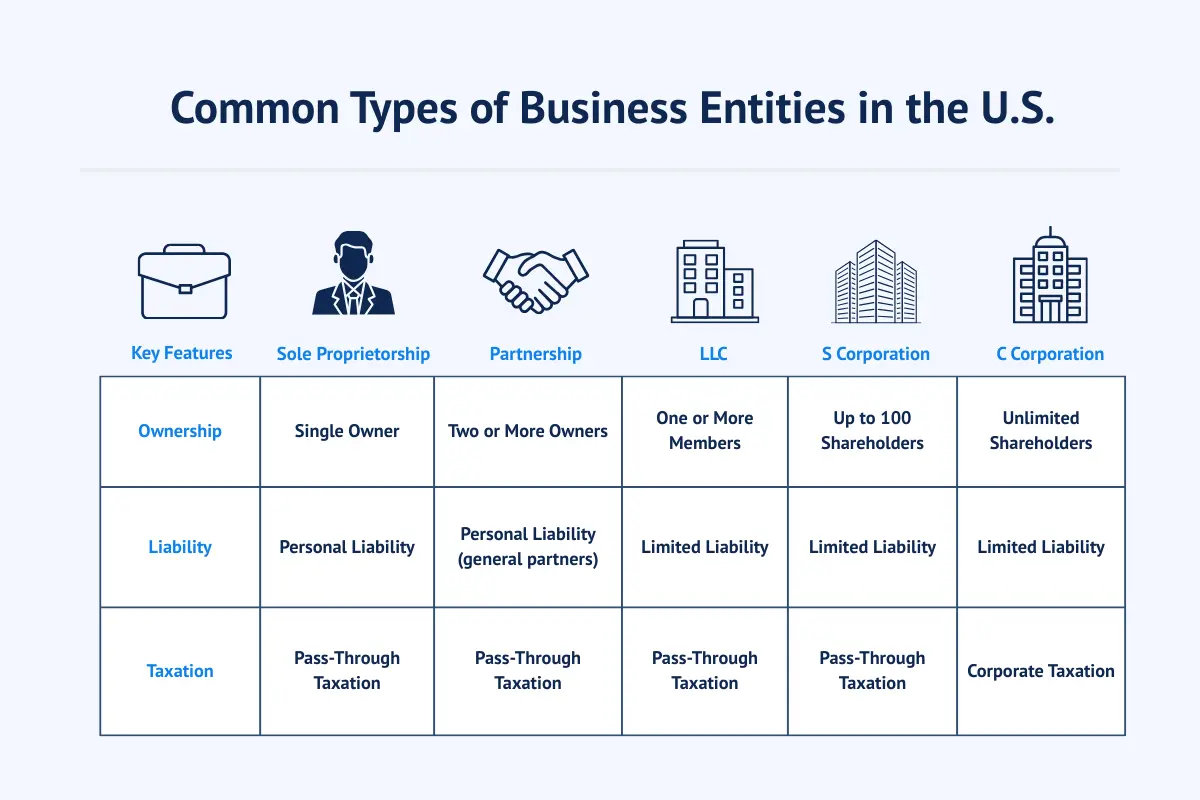

When evaluating what are the 4 types of business structures, the most common U.S. business entity types include sole proprietorships, partnerships, LLCs, and corporations. Each represents a different legal structure under which a business is formed and recognized by state and federal authorities. This article provides a high-level comparison of these structures, focusing on general differences in organization, liability, and compliance rather than recommendations or legal advice.

Entity type decisions typically occur before filing formation documents. Understanding business entity identifiers helps distinguish between different classification systems. The United States currently has a large number of pass-through businesses, which pay taxes through the individual income tax code rather than the corporate code, according to the Tax Foundation. Pass-through entities represent approximately 73% of businesses in the United States. These sole proprietorships, S corporations, and partnerships account for more than half of net business income in America.

Key Takeaways

-

Choosing a business entity type shapes how a business is formed, owned, managed, taxed, and dissolved, so it should be evaluated before filing any formation documents.

-

The most common U.S. business structures are sole proprietorships, partnerships, LLCs, and corporations, with some variations such as S corporations and nonprofit corporations.

-

Sole proprietorships and general partnerships are easy to start and use pass-through taxation, but they do not provide personal liability protection for business debts or legal claims.

-

LLCs and corporations are separate legal entities that can offer limited liability protection when properly formed and maintained, but they require formal state filings and ongoing compliance.

-

Different entity types have different default tax treatments and available elections, so the same legal structure can be taxed in multiple ways depending on elections made with the IRS.

-

Pass-through entities such as sole proprietorships, partnerships, and S corporations account for the majority of U.S. businesses and a large share of total business income.

-

Formation and ongoing compliance requirements—including annual reports, registered agent designation, and recordkeeping—vary by state and entity type, affecting administrative complexity and cost.

What Is a Business Entity Type?

A Business Structure type is the legal structure under which a business is formed and recognized by state and federal authorities. This classification establishes the framework for ownership, management, liability, and taxation.

Business Entity Types do not automatically guarantee specific benefits. Actual legal and tax treatment depends on state law, federal regulations, how entities are formed, and how they are maintained. Choosing an entity type affects the legal framework within which businesses operate.

Different jurisdictions recognize different entity types with varying requirements. What qualifies as valid in one state may have different rules in another. The specific laws of the jurisdiction of formation govern formation and ongoing obligations.

Why Entity Type Matters Before You Form a Business

The selected entity type influences liability exposure, tax treatment, governance requirements, and ongoing Compliance requirements. These structural differences affect how businesses operate and what obligations entities must fulfill.

Liability exposure varies among entity types. Some structures provide separation between business obligations and owners' personal assets when properly formed. Others offer no such separation, leaving owners exposed to business debts.

Tax treatment differs based on entity classification. Some entities are taxed at the entity level, while others allow income to pass through to owners. Outcomes vary by individual circumstances.

Common Types of Business Entities in the U.S.

The following types of business entities, with examples, provide general explanations of commonly recognized U.S. business entity types. Availability and specific rules are governed by state and federal law. These are informational overviews, not recommendations.

State laws determine which entity types are available. Some structures require formal state registration, while others form by default. Understanding baseline characteristics helps business owners evaluate options.

Sole Proprietorship

A Sole Proprietorship structure represents a single-owner business that is not legally separate from its owner. This form typically requires no state-level entity registration. The business and its owner are treated as a single entity for legal and tax purposes.

Sole Proprietorship businesses report income directly on owners' personal tax returns using Schedule C. No separate business tax return is required. Owners pay self-employment taxes on business income.

The lack of a Legal separation between the business and the owner means business obligations can affect personal assets. Creditors with claims against businesses may pursue owners' personal property to satisfy debts.

General Partnership

A General Partnership is a business operated by two or more owners, which may be formed by agreement or by default under state law. No state registration is typically required, though some jurisdictions require trade name filings.

Partners share management authority and responsibility. Each partner can typically bind the partnership to contracts. This creates mutual exposure to business decisions made by any partner.

Similar to sole proprietorships, general partnerships provide no legal separation between business obligations and partners' personal assets. Limited partnership structures offer different liability allocations through formal state registration.

Limited Liability Company (LLC)

A Limited Liability Company (LLC) is a separate legal entity that can provide limited liability protection when properly formed and maintained under state law. LLC formation requires filing organizational documents with state authorities.

Limited Liability Company (LLC) structures feature flexible management options. Members can manage LLCs directly or appoint managers. Ownership structure can accommodate single owners or multiple members with varying percentages.

Limited Liability Company (LLC) entities can elect different tax classifications. By default, single-member LLCs are disregarded entities while multi-member LLCs are taxed as partnerships. LLCs can elect corporate taxation by filing forms with the IRS.

Corporation (C Corporation and S Corporation)

A corporation is a separate legal entity with a formal governance structure including shareholders, directors, and officers. Corporations are formed at the state level through articles of incorporation. Corporate structures separate ownership from management.

C corporations face entity-level taxation on profits, and then shareholders pay individual income tax on dividends. S Corporation status is a tax classification, not a separate entity type.

An S corporation election allows profits to pass through to shareholders' personal tax returns. The entity itself does not pay federal income tax. Specific eligibility requirements limit which entities can elect S corporation status.

Nonprofit Corporation

Nonprofit organizations are purpose-driven entities formed for charitable, educational, religious, or similar missions. Cornell Law School explains that nonprofit corporations face additional state and IRS requirements beyond those applying to for-profit entities.

Nonprofit formation requires articles specifying charitable purposes. Organizations seeking tax-exempt status must apply to the IRS separately. Nonprofits cannot distribute profits to members as dividends. Any surplus revenues must further charitable missions.

Key Differences Between Business Entity Types

When considering what are the 3 types of business entities most commonly formed (sole proprietorships, partnerships, and LLCs), or expanding to include corporations, entity types vary across multiple dimensions affecting formation, operation, and ongoing obligations. These differences create distinct frameworks within which businesses function. Understanding key distinctions helps clarify why entity selection matters.

Comparing entity characteristics requires examining multiple factors simultaneously. No single factor determines which structure suits particular situations. Legal requirements, tax treatment, administrative burdens, and operational flexibility all contribute to the overall framework each entity type creates.

Legal Separation and Liability Exposure

Different entity types vary in whether and how businesses are legally distinct from their owners. Sole proprietorships and general partnerships create no legal separation. Business obligations directly affect owners personally. Creditors can pursue owners' personal assets for business debts.

Corporations and LLCs may provide limited liability protection when properly formed and maintained. These structures create legal entities separate from owners. Business obligations generally attach to entities rather than owners personally. Liability outcomes depend on entity structure, state law, proper formation, and ongoing compliance.

Legal separation is not absolute, even for corporations and LLCs. Courts may disregard entity structures in cases involving fraud, inadequate capitalization, or failure to maintain corporate formalities. Owners signing personal guarantees for business obligations remain personally liable regardless of entity type.

Tax Classification and Reporting

Entity types differ in default federal tax treatment and available elections. Sole proprietorships and general partnerships are "pass-through" entities, meaning income flows to the owners' personal returns. No entity-level taxation occurs. Owners report business income as personal income.

Corporations face entity-level taxation under default C corporation treatment. Corporate income is taxed at the entity level, and then dividends are taxed when distributed to shareholders. The IRS explains that S corporation status represents a tax election rather than a separate entity type.

LLCs can elect how they are taxed. Single-member LLCs are disregarded entities by default. Multi-member LLCs default to partnership taxation. LLCs can elect corporate taxation if beneficial. These elections affect reporting obligations and overall tax treatment.

Ownership and Management Structure

Entity types differ in Ownership structure rules, decision-making authority, and governance requirements. Sole proprietorships have a single owner who directly controls all business decisions. No formal governance structure is required. Owner authority is complete and unrestricted.

Partnerships involve shared ownership and typically shared management authority. Partnership agreements can specify different management allocations among partners. Some partners may have more authority than others under the terms of the agreement.

Corporations separate ownership from management through the roles of shareholders, directors, and officers. Shareholders own equity but do not directly manage operations. Directors provide oversight while officers handle daily management. This layered structure creates formal governance frameworks.

Formation and Administrative Requirements

Entity types differ in the steps required for formation, the required filings, and the initial setup complexity. Sole proprietorships and general partnerships typically require no formal state registration. Businesses can begin operating without filing organizational documents. However, local business licenses may still be required.

Corporations, LLCs, and limited partnerships require filing organizational documents with state authorities. Articles of incorporation or organization must be prepared and submitted, along with the appropriate fees. Formation procedures are governed by state law and vary by jurisdiction.

State filing procedures differ in complexity, cost, and processing time. Some states offer online filing with immediate confirmation. Others require paper filings with longer processing periods. Required information and fee structures vary substantially across jurisdictions.

Ongoing Compliance and Maintenance

Entity types differ in recurring obligations such as annual reports, registered agent requirements, and recordkeeping expectations. Understanding annual report requirements helps entities maintain good standing with formation states.

Corporations typically face more extensive ongoing requirements than other structures. Annual meetings, meeting minutes, and formal recordkeeping help maintain corporate formalities. Failure to observe these requirements can jeopardize liability protections.

LLCs generally have fewer ongoing formalities than corporations but more than sole proprietorships or general partnerships. Most states require annual reports and the maintenance of a registered agent. Specific requirements vary by state and entity type.

Flexibility and Long-Term Considerations

Entity types differ in their adaptability over time, particularly with respect to ownership changes, structural adjustments, and conversions. Some structures accommodate ownership transfers more easily than others. Corporations can issue and transfer stock relatively simply, facilitating ownership changes.

Partnership structures may require amendments to the partnership agreement when ownership changes. Some partnership agreements dissolve the partnership when a partner exits. Others include provisions for continuing operations with remaining partners.

Entities can convert from one structure to another in most jurisdictions, though processes and implications vary. Conversions may trigger tax consequences or require dissolution and reformation. Professional guidance often accompanies structural changes.

Factors Business Owners Commonly Consider When Comparing Entity Types

Business owners evaluate multiple factors when comparing entity options. These considerations help narrow choices based on individual circumstances. No single factor determines appropriate selection for all situations.

Different factors carry different weights depending on specific business characteristics and long-term plans. Professional advisors often help owners prioritize considerations.

Ownership Structure

Entity types differ in who can own businesses and how ownership interests are defined. Sole proprietorships have single owners. Partnerships require two or more owners. Corporations and LLCs can have one or more owners.

Some entity types impose ownership restrictions. S corporations limit the number and type of shareholders. Nonprofit corporations prohibit traditional ownership interests. These restrictions affect which structures accommodate specific ownership preferences.

Ownership rules are set by entity type and state law. Some states impose additional requirements beyond federal rules. Understanding applicable ownership limitations helps identify viable entity options.

Management Preferences

Business entity management types vary in day-to-day management and decision-making frameworks. Owner-managed models allow owners direct control over all business decisions—more formal governance structures separate ownership from management.

Some owners prefer active involvement in daily operations. Others prefer passive investment roles with professional managers handling operations. Entity selection should align with the desired level of management involvement.

Governance preferences evolve as businesses grow. Structures suitable for single-owner startups may not accommodate multiple investors with varied management interests. Long-term management plans factor into entity selection.

Administrative Complexity

Entity types differ in the steps for formation, recordkeeping expectations, and filing requirements. Simpler structures involve less paperwork and fewer ongoing obligations. More complex structures require greater administrative attention.

Administrative obligations differ by entity type and jurisdiction. Some states have streamlined online filing systems, while others require paper submissions. Processing times and fee structures vary substantially.

Administrative burdens are ongoing commitments throughout an entity's lifespan. Maintaining legal identity requires consistent attention to compliance obligations regardless of business size or success.

State-Level Compliance Obligations

Ongoing compliance requirements, such as annual reports, registered agent designation, and state fees, are governed by the laws of the state where the entity is formed. Compliance obligations attach to business entities themselves, not owners.

Requirements vary depending on the formation jurisdictions. States impose different filing schedules, fee structures, and information requirements. Multi-state operations face compliance obligations in each jurisdiction where entities are registered.

Failure to meet state compliance obligations can result in administrative dissolution or loss of good standing. These consequences affect entities' ability to conduct business legally and maintain liability protections.

Legal and Tax Considerations to Be Aware Of

Entity type selection can affect legal responsibilities, tax classification, and reporting obligations. Outcomes depend on individual facts and applicable jurisdiction laws.

Legal and tax implications extend beyond initial formation. Ongoing operations and business transactions are subject to legal and tax rules. Business owners often consult licensed attorneys for legal guidance and certified public accountants for tax advice.

How Professional Formation and Compliance Support Can Help

Professional services assist with the accurate preparation and filing of formation documents. Registered agent representation helps ensure entities receive important legal notices when applicable. Ongoing compliance tracking helps reduce risks of missed deadlines.

InCorp provides business filing and compliance support that helps reduce administrative burden and improve efficiency. Professional support does not replace owners' ultimate responsibility for legal compliance or tax obligations. Services complement rather than substitute for professional legal or accounting advice.

Comparing entity types helps identify structural differences before formation. Professional formation services help ensure documents are prepared correctly and filed properly with the appropriate authorities.

Next Steps After Knowing About Entity Types

Understanding different business entity types provides a foundation for evaluating formation options. Entity characteristics create frameworks within which businesses operate. Entity selection depends on individual circumstances and professional advice from qualified advisors.

Starting a business involves multiple steps beyond entity selection. Formation documents, tax registrations, licenses, and compliance systems all contribute to the proper establishment of a business.

FAQ's

How is an LLC different from a corporation?

An LLC typically offers flexible management and pass-through taxation by default, while corporations follow a more formal structure with shareholders, directors, and officers, and may be subject to different tax treatment. Both can provide limited liability protection when properly formed and maintained.

What is the simplest business entity to form?

A sole proprietorship is generally considered the simplest entity because it does not require formal state-level formation filings in most states. However, simplicity in formation does not necessarily mean simplicity in ongoing operations or tax treatment.

Do all business entities provide liability protection?

No. Sole proprietorships and general partnerships do not provide personal liability protection, while LLCs and corporations generally offer limited liability when properly formed and maintained. Liability protection depends on entity structure, proper formation, and ongoing compliance with applicable requirements.

Can a business change its entity type later?

Yes. Many businesses convert or restructure their entity type as they grow, though the process and implications vary by state and entity. Conversions may involve tax consequences, dissolution and reformation procedures, or other complexities requiring professional guidance.

What is the difference between a general partnership, a limited partnership, and a limited liability partnership?

In a general partnership, two or more persons share management and are usually personally liable for partnership debts and business decisions. A limited partnership includes at least one general partner with full management authority and personal liability, and one or more limited partners who typically have limited personal liability but reduced management rights. A limited liability partnership can offer partners liability protection for certain obligations, subject to state rules, while still being treated as a partnership for many tax and management purposes.

How do corporations (C corporations and S corporations) compare to other business structures for taxes and raising capital?

A C corporation is an independent legal entity that can issue stock, raise funds from multiple investors, and may face double taxation: corporate taxes on profits and then individual taxes on dividends. An S corporation is a corporation that elects a special tax status under the Internal Revenue Code so that eligible small business owners report profits and losses on their personal tax returns, avoiding corporate-level income tax in many cases. Both forms of corporation can be attractive for raising capital but have more formal management structure and compliance requirements than many other business entities.

When might a nonprofit corporation be the right type of business entity?

Nonprofit organizations and charitable organizations often choose a nonprofit corporation form of business when their primary purpose is educational, religious, charitable, or similar and not to distribute profits to owners. A nonprofit corporation exists separately from its founders, can hire employees, and may seek tax exempt status from the Internal Revenue Service if it meets specific requirements. Unlike other structures, any surplus generally must support the organization's mission rather than being paid out as profits to owners.

Why should business owners talk to a business attorney or tax professional before choosing an entity type?

Different entity types offer different legal protections, tax benefits, and obligations, and the best business structure depends on specific business activities, ownership goals, and long-term plans. A business attorney can explain liability protection, corporate formalities, partnership agreement terms, and state rules for transferring ownership, while a tax professional can address federal taxes, tax filing requirements, and how profits and losses will appear on owners' personal income tax returns. Professional guidance helps small business owners avoid costly restructuring if they later discover another structure would have better matched their needs.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.