What Is a UCC Search and How It Works in Business Records

A business owner negotiating equipment financing learned at closing that another lender already held priority claims on the same assets being pledged as collateral. The new lender discovered this through routine due diligence, which forced the renegotiation of loan terms and delayed the transaction by weeks. Without understanding what a UCC search is and its role in revealing existing claims, both parties faced unnecessary complications and increased transaction costs.

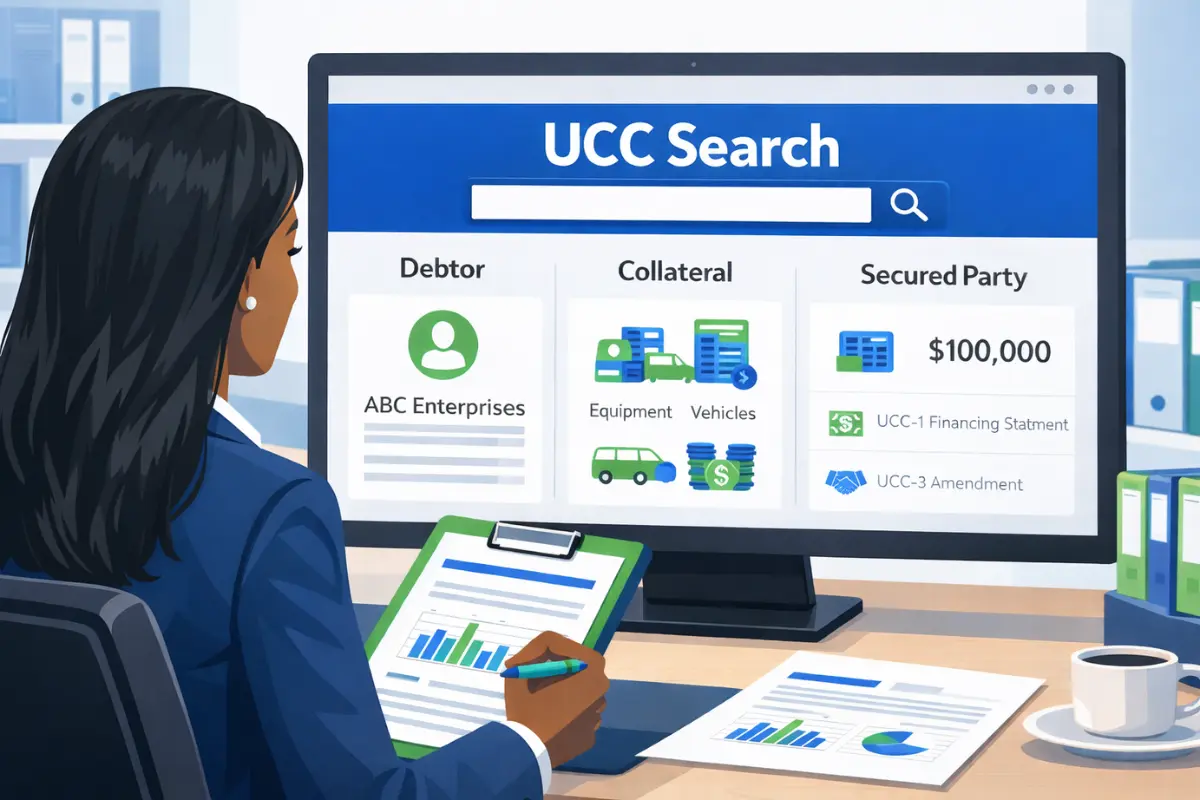

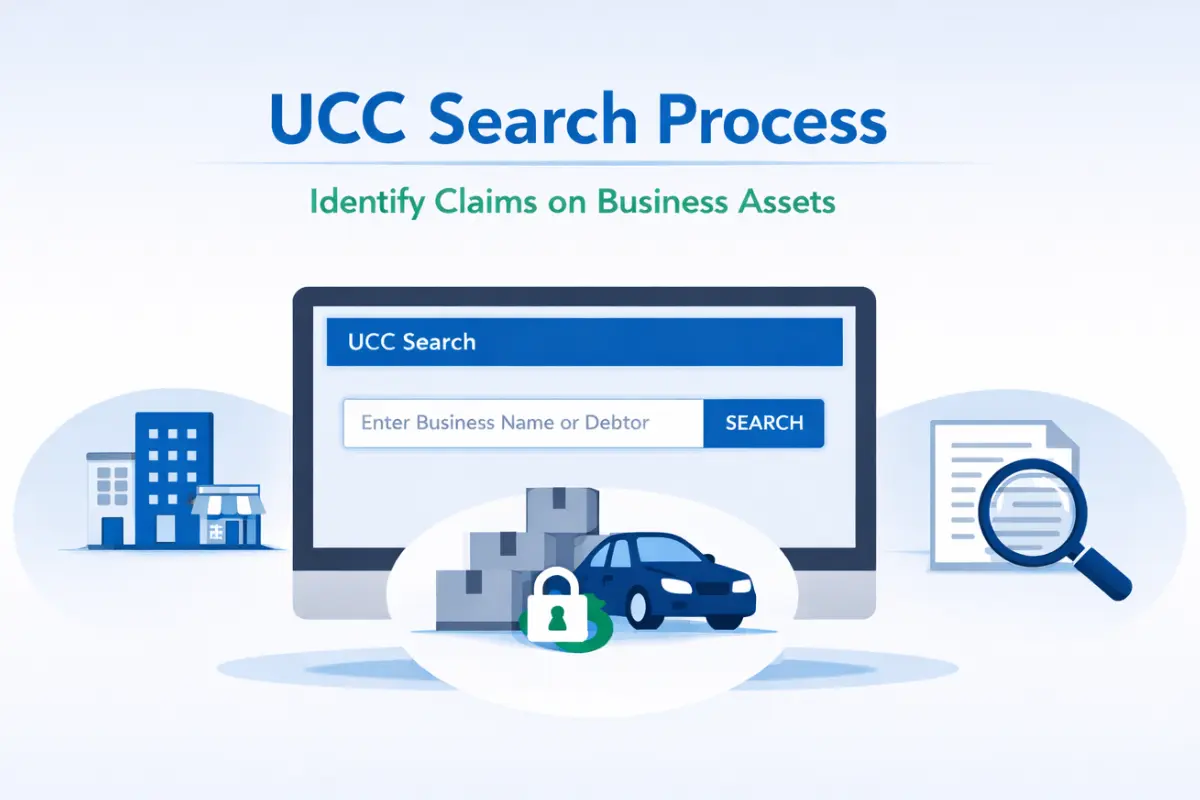

A UCC search involves looking up public records related to secured transaction records filed under the Uniform Commercial Code. These searches reveal whether lenders have filed claims against business assets, helping parties assess potential risks before extending credit or completing transactions. Understanding how UCC searches work supports informed decision-making in lending and business dealings.

Businesses use UCC searches to identify existing security interests before entering financial arrangements. Lenders review these records to evaluate asset availability, while buyers conducting due diligence check for encumbrances that might affect acquisition values. The search process provides factual information about recorded claims, though interpretation requires careful consideration within broader transaction contexts.

Key Takeaways

-

A UCC search reviews public records of secured transactions to identify existing liens or security interests on a business’s personal property before loans or major deals proceed.

-

The most common UCC filings you will see in search results are UCC-1 financing statements (which create public notice of a security interest) and UCC-3 filings (which amend, continue, or terminate an existing record).

-

Lenders, buyers, and investors use UCC searches as part of due diligence to evaluate collateral availability, understand creditor priority, and spot potential complications before closing a transaction.

-

UCC search results typically show the debtor’s legal name, the secured party, collateral description, filing date, and current status, but they do not reveal every possible liability or guarantee asset availability.

-

Because UCC rules and priority issues can be technical and fact-specific, businesses should treat searches as one component of a broader risk review and consult qualified professionals for legal or financial advice when interpreting results.

Types of UCC Filings You May See

UCC filing search results typically show two main document types: UCC-1 statements that establish initial security interests and UCC-3 amendment termination documents that modify or terminate existing filings. Texas Secretary of State filing instructions provide detailed guidance on these document types and their functions within the state's public record system.

UCC-1 financing statements create the first public record of lenders' claims on business assets. UCC-3 documents serve various purposes, including amendments, terminations, and continuations of existing records. Each document type serves specific functions in the filing process, with different requirements and effects on public records.

Understanding these filing types helps parties interpret search results accurately. Not all filings indicate current obligations; terminated filings show resolved debts, while active filings may represent standard business financing arrangements rather than financial distress.

UCC-1 – The Original Financing Statement

The UCC-1 financing statement creates the initial public record of secured parties' claims against the debtor's assets. Lenders file these documents with the Secretary of State offices where debtors are incorporated or where collateral is located. Filings typically occur when loans are extended, and borrowers grant security interests in business property.

UCC-1 statements identify debtors by legal names, name secured parties holding interests, and describe collateral securing obligations. Collateral descriptions may be specific or general, covering all assets of certain types.

These filings remain effective for five years from filing dates unless terminated earlier or continued before expiration.

UCC-3 – Changes to an Existing Filing

UCC-3 documents modify or terminate previously filed UCC-1 statements rather than creating new security interests. These filings reference original UCC-1 file numbers, linking amendments or terminations to specific existing records.

The filing process for UCC-3 documents requires proper authorization from secured parties. Only parties holding security interests or their authorized representatives can file amendments or terminations.

UCC-3 filings serve multiple purposes, including updating debtor information, modifying collateral descriptions, assigning security interests to new parties, and terminating completed transactions.

UCC-3 Amendment

Amendments update information in existing UCC-1 statements without terminating underlying security interests. Common amendments change debtor names after business name changes, update secured party information following lender mergers, or modify collateral descriptions. Amendments keep original filings active while reflecting current information.

Understanding UCC filings helps businesses recognize when amendments become necessary. Name changes or entity restructuring may require filing amendments to keep public records accurate.

Amendments do not reset filing dates or extend expiration periods.

UCC-3 Termination

Terminations remove lenders' security interests from public records after debts are paid. Secured parties file termination statements confirming obligations are satisfied and releasing claims on collateral.

Terminated filings remain visible in UCC public records but are marked as inactive. Search results display termination dates alongside original filing information.

Borrowers should promptly confirm the termination of secured parties' files after loan payoffs. Document retention guidelines help businesses maintain records of terminations for future reference.

UCC-3 Continuation

Continuations extend the effectiveness of UCC-1 filings before their five-year terms expire. Secured parties file continuations within six months before expiration dates, extending effectiveness for an additional five-year period.

If secured parties fail to file continuations before expiration, filings lapse and no longer provide public notice of security interests. Timely continuation filing prevents gaps in public records.

Continuations do not modify underlying security interests, they simply extend public notice periods.

Why Businesses and Lenders Use UCC Searches

Lenders use UCC lien lookup services to assess risks before extending credit. Buyers and partners use searches during due diligence when evaluating business transactions. Understanding how public filing data supports business decisions demonstrates the strategic value of systematic research into public records.

UCC searches form one component of comprehensive due diligence processes. While they reveal filed security interests, searches do not capture all potential liabilities or guarantee the availability of assets. Parties combine UCC searches with tax lien searches, litigation searches, and other investigations to develop complete risk assessments.

Risk Management strategies incorporate UCC searches as standard procedures in lending and acquisition workflows. Regular search protocols help organizations identify potential complications before finalizing commitments, supporting more informed decision-making throughout transaction processes.

To Identify Existing Claims Before Lending

Lenders review commercial lien search results to determine whether borrowers' assets are already pledged to other creditors. Discovering existing security interests helps lenders evaluate whether sufficient unencumbered collateral remains to secure new loans.

Multiple UCC filings against businesses may indicate either active use of asset-based financing or potentially overleveraged conditions. Context matters—healthy businesses commonly pledge assets to multiple lenders for different purposes.

Legal and Financial Professionals advise clients that UCC searches reveal only what has been filed, not necessarily what exists. Unfiled security interests or security interests perfected through possession may not appear in searches yet still affect priority.

To Support Due Diligence in Business Transactions

Buyers and investors use UCC searches when evaluating acquisition targets or investment opportunities. Search results help parties understand what assets may remain encumbered after transactions close.

Business due diligence search practices extend beyond UCC searches to include comprehensive reviews of corporate records and compliance status.

Searchers reviewing acquisition targets should consider whether existing UCC filings will be paid off at closing or assumed by buyers.

To Understand Priority of Security Interests

Filing timing affects which creditors have priority when multiple parties claim interests in the same collateral. Earlier-filed UCC-1 statements generally have superior priority over later filings, though exceptions exist.

Priority rules involve complex legal advice that requires professional interpretation. Purchase money security interests and statutory liens may override general first-to-file rules.

Maintaining good standing helps businesses secure favorable financing terms over time.

To Reduce Uncertainty Around Asset Obligations

UCC searches help parties understand whether assets may be restricted by existing security arrangements. This awareness supports informed decisions rather than guaranteeing specific outcomes. Search results provide factual information about filed claims, though actual asset availability depends on many factors that searches cannot reveal.

Parties should recognize that UCC searches show only what secured parties chose to file. Inaccurate filings, expired filings not yet removed from indexes, or filings with errors may appear in results. Careful review and verification help parties avoid misinterpreting search findings.

Business record-keeping practices should include maintaining copies of UCC filings affecting business assets. Organized records help businesses track which assets are pledged, when filings expire, and what actions are needed to maintain or release security interests.

What Information a UCC Search Reveals

UCC public records searches return information about debtors, secured parties, collateral descriptions, filing dates, and current status. Results show what has been filed in searched jurisdictions, but do not verify the accuracy or current relevance of information. Public filing data analysis reveals patterns and insights supporting business strategy development.

Search results display only information contained in filed documents. Filers control what information appears in public records through their filing submissions. Errors in debtor names, secured party identifications, or collateral descriptions may cause searches to miss relevant filings or return incorrect information.

Interpreting search results requires understanding what information means within broader transaction contexts. Multiple filings may indicate active business operations using asset-based financing rather than financial distress. Single filings may represent either minor loans or major financing arrangements, depending on the scope of collateral.

The Legal Name of the Debtor

Searches return results based on exact matches of the debtor name in filing office indexes. The legally registered name of businesses or individuals appears in search results exactly as filed. Name accuracy proves important because slight variations can cause searches to miss relevant filings.

Businesses should search under current legal names and any former names used during relevant periods. Entity name changes, mergers, or restructurings may result in filings under multiple names. Comprehensive searches check all name variations to avoid missing relevant security interests.

Personal Property Security Act provisions in some jurisdictions require specific formats for debtor names. Understanding jurisdictional requirements helps searchers identify proper search terms and interpret results correctly within applicable legal frameworks.

The Secured Party on Record

Search results list secured parties holding filed security interests in debtors' assets. These parties may be lenders, equipment lessors, or other creditors that hold security interests under lending or credit arrangements. Secured party information identifies who filed claims and who might assert rights to collateral.

Secured parties may assign security interests to other parties without necessarily filing amendments. Search results may not reflect current secured party identities if assignments occurred without recorded amendments. Parties relying on search results should verify current secured party information when relevant to significant transactions.

Multiple secured parties appearing in the results indicate that the debtor's assets are pledged to various creditors. The number and nature of secured parties provide context about debtor financing arrangements and potential complications in asset-based lending or business acquisitions.

The Collateral Description

The filed documents outline which assets are subject to security interests. Collateral descriptions range from specific (identifying particular pieces of equipment by serial number) to general (covering all inventory, equipment, or accounts receivable). The scope of description determines how much of the debtor's property is encumbered.

Broad collateral descriptions like "all assets" or "all personal property" indicate that substantial portions of a business's assets are pledged. More limited descriptions covering specific equipment or inventory categories leave other asset types potentially available for additional financing. Searchers assess collateral scope to evaluate asset availability.

Judgment lien searches conducted alongside UCC searches provide a more complete picture of asset encumbrances. While UCC filings cover consensual security interests, judgment liens represent non-consensual claims that may also affect asset availability and creditor priorities.

The Filing Date and Status

Results show when security interests were filed and whether filings remain active, have been terminated, or have lapsed. Filing dates establish when security interests were perfected, affecting priority among competing creditors. Earlier filing dates generally indicate higher priority.

Current status information distinguishes active filings from terminated or expired ones. Active filings indicate continuing security interests, while terminated filings show resolved obligations. Lapsed filings that expired without continuation no longer provide public notice but may indicate historical financing patterns.

Timing affects how long claims may remain on record. Legal notice requirements provide that UCC-1 filings remain effective for five years unless continued. Understanding duration rules helps parties assess whether active filings reflect current obligations or outdated records that need administrative cleanup.

Get Clear on UCC Searches Before Your Next Business Decision

What is a UCC Search can be summarized as the process of reviewing public records to identify filed security interests affecting business assets. These searches help lenders, buyers, and other parties identify existing claims before extending credit or completing transactions. While searches provide valuable information, they are only one component of comprehensive due diligence, not a complete risk assessment tool.

Understanding what searches reveal, and what they do not, helps parties use this information appropriately. Search results show only what has been filed in specific jurisdictions searched, using specific debtor names provided. Unfiled interests, filings in other jurisdictions, or filings under name variations may not appear in limited searches.

InCorp provides professional registered agent services and compliance support, helping businesses maintain organized records and meet state requirements. Contact InCorp to learn how administrative support services help businesses manage regulatory obligations and maintain accurate public records supporting efficient business operations.

FAQs

Are UCC searches public information?

Yes. UCC filings are part of public state records, and most filing offices (often the Secretary of State) provide online search tools that anyone can use to look up UCC records under a business name or individual debtor name. Because these indexes are public, lenders, buyers, and other parties routinely use UCC searches during due diligence to identify existing liens or security interests before extending credit or closing transactions.

Can an individual person have a UCC filing against them?

Yes. A UCC filing can name an individual as the debtor if that person has granted a security interest in personal property, such as equipment, inventory, or other assets, to secure a loan or line of credit. As with business debtors, filings for individuals use the debtor's exact legal name as it appears on official identification, and accurate naming is critical to ensure searches capture all relevant records.

Do UCC filings expire on their own?

Most UCC-1 financing statements are effective for five years from the filing date and then lapse automatically unless a continuation statement is filed within the six months before the scheduled lapse date. Once a filing lapses, it generally no longer serves as public notice of a perfected security interest, although the underlying obligation may still exist and other perfection methods may apply in some circumstances.

Can there be more than one UCC filing on the same business?

Yes. It is common for a business to have multiple UCC filings if different creditors hold security interests in different collateral or in overlapping categories of assets. When reviewing UCC search results, lenders and legal teams consider filing dates, collateral descriptions, and any continuation statements to evaluate which secured parties may have priority in specific assets.

Does a UCC filing affect a business's credit score?

A UCC filing itself does not typically change a business's credit score in the same way as payment history or delinquencies, but lenders may take UCC filings into account when assessing overall credit risk. Multiple active filings can indicate that a borrower's assets are already pledged to other creditors, which may influence decisions about extending additional credit or the terms offered.

What is the difference between a UCC search and a tax lien search?

A UCC search looks for secured transactions recorded under the Uniform Commercial Code, showing voluntary security interests that creditors have in a debtor's personal property. A tax lien search focuses on statutory claims filed by government agencies (such as the IRS or state tax authorities) for unpaid taxes, which can also encumber assets but arise independently of UCC financing statements.

Where is a UCC search usually conducted for a business?

For most entities, UCC searches are performed in the central state filing office, often the Secretary of State in the state where the debtor is organized or, for individuals, in the state of their principal residence. Depending on the collateral and legal requirements, additional searches may be appropriate in other jurisdictions or specialized filing systems to capture all relevant records.

Why does the debtor's exact legal name matter so much in a UCC search?

UCC indexes are typically organized by the debtor's exact legal name, so even small differences—such as missing middle names, extra initials, or spelling errors—can cause a search to miss important filings. Using the precise legal name from formation documents for entities, or from government-issued identification for individuals, helps ensure the search results accurately reflect all filed UCC records.

What is a certified UCC search and when is it used?

A certified UCC search is an official report issued by the filing office that lists all UCC records indexed under a specified debtor name as of a particular date and time, often with a certification or seal. Certified searches are commonly requested in larger or higher-risk transactions so that lenders, buyers, and legal teams can rely on a formal record from the filing office for closing and documentation.

Does a UCC filing mean the debt is still outstanding if the loan has been paid off?

Not always. A UCC filing may remain active in the public index even after a secured obligation has been fully satisfied if the secured party has not filed a termination statement. Because of this, parties reviewing search results often confirm with the creditor whether a listed filing reflects an existing secured interest or a loan that has already been paid in full.

Disclaimer: This content is intended for general educational and informational purposes only and does not constitute legal, tax, or accounting advice. Every effort is made to keep the information current and accurate; however, laws, regulations, and guidance can change, and no representation or warranty is given that the content is complete, up to date, or suitable for any particular situation. You should not rely on this material as a substitute for advice from a qualified professional who can consider your specific facts and objectives before you make decisions or take action.

Share This Article:

Stay in the know!

Join our newsletter for special offers.